Top 5 Investor Concerns: Don’t Get Spooked!

Black swan events are justifiably defined as rare, unexpected and catastrophic occurrences that are impossibly difficult to predict.

Finance professor and author Nassim Nicholas Taleb describes a black swan (in his book of the same moniker) as an event that 1) is beyond normal expectations that is so rare that even the possibility that it might occur is unknown, 2) has a catastrophic impact and 3) is explained in hindsight as if it were actually predictable.

Black Swan events are becoming more frequent rather than being a rarity, from the dot.com crash (2000), 9/11 Terrorist Attacks (2001), Global Financial & housing Meltdown (2008), Zimbabwe 79.6% hyperinflation (2008), Fukushima Nuclear Disaster (2011), Crude Oil Crash (2014), Black Monday China (2015), Brexit (2016) and the COVID19 Pandemic (2020). These events seem to tie financial and non-financial events together with a reach affecting people globally well beyond Wall Street.

While you may not be able to predict a Black Swan event, you can nonetheless put a contingency plan in place for your portfolio like installing impact-proof windows to your house if you are concerned about future hurricanes. At the same time, many of our top five investor concerns for Q4 are not Black Swan events per se, as they are known financial events brewing that may possibly come to realization. Whether they will cause a short term or more troublesome, longer term economic and market effect is unknown.

Top 5 Investor Concerns for Q4

1. US Debt Default: Congress is seeking to delay the debt ceiling debacle until December 3rd by voting to raise the nation’s borrowing limit by $480 billion to stave off default and provide a couple more months to debate over President Biden’s 2,465 page, ten-year “Build Back Better” $3.5 trillion social policy plan. Failure to raise the debt ceiling could result in a financial meltdown.

2. China Economic Crisis: The impending default later this month of an $83 Million interest payment due by Chinese top property developer Evergrande on it’s $300 Billion in debt is raising concerns about a potential liquidity crisis among all Chinese and Hong Kong property companies, leading up to a potential financial crisis that could seep into other world economies.

3. Fed Tapering & Rates: The Fed is likely to begin reducing its $120 billion per month in government backed bond purchases this quarter, which have pumped trillions of dollars of cash into the financial markets since the COVID19 crisis started in 2020. While this policy has supercharged growth and stocks, cutting off this cash-infused “i.v.“ and ultimately hiking interest rates could create new unique economic repercussions.

4. Tax Hikes: There are concerns that individual and corporate tax hike proposals to help pay for President Biden’s proposed $3.5 trillion social/ budget bill could derail the economy, jobs and corporate profits, while passing along a good bit of the costs to consumers in the manner of higher prices for goods and services and added inflation.

5. Inflation: Ominous headlines hyping the biggest inflation scare in 40 years is forming and will wreak havoc on consumer goods, interest rates and the stock market, appears to be the “theme du jur” this year. Whether the recent surge in demand following the “supply shock” rebound out of the economic shutdown will take us back in time to the disco days of the 70’s, or cool off a bit, is unknown.

Navigating Investor Concerns

As we begin the final quarter of 2021, the economy is shifting from a recovery phase to a sustained expansion. Investor sentiment has shifted alongside this, swinging from bullishness to bearishness. This is understandable because, while the underlying trends are positive, it’s no longer the case that the economy and markets have nowhere to go but up.

Challenges such as the pace of growth, fears of stagflation, China economic problems, Fed policy, the debt ceiling, “supply-side” chain-issue problems and more are weighing on investors’ minds and do arise in our client service meeting conversations. How can investors balance risk and reward with a long-term perspective during the final months of the year?

The truth is that investing is never easy except in hindsight. In the moment, there are always concerns that worry investors, even when they have a sound financial plan and portfolio strategy. Just this year alone there have been other polarizing topics as far ranging as the presidential transition to the Delta variant and Afghanistan. Yet, the S&P 500 pushes forward. The markets repeatedly show that those who are able to stay disciplined and look past the daily headlines are often rewarded, regardless of how quickly market sentiment turns.

Today, the big issues that weigh on markets can seem nearly insurmountable, as they often do. The nature of the short recession last year, which only lasted two months, and the swift recovery have been unlike any cycle in history. This has made it difficult to measure and interpret traditional economic data such as inflation and growth rates.

On top of measurement and interpretation issues, there have also been real structural challenges, most notably around global supply chains. Much of this is rooted in the on-going disruptions in manufacturing and shipping that have affected industries from semiconductors to construction materials. While it’s reasonable to expect that these issues will be resolved, trying to predict the exact timing is difficult if not impossible from computer chips to lumbar.

Perhaps then the biggest shift in markets over the past several weeks is that interest rates have begun to rise after pausing for two quarters. This has put downward pressure on bonds to tech-related sectors, counter-balancing improvements in areas such as energy and financials. Not only will interest rates likely climb further, but investors should continue to expect elevated levels of volatility.

It’s important to emphasize that this is all occurring against a backdrop of a strong economy and robust corporate profits – factors that do not depend on how investors feel. Ultimately, long-term investors ought to position themselves for years and decades, not days, weeks or months. By most measures, we are still early in the business cycle despite the shared feeling that the pandemic has lasted a lifetime already. Achieving financial goals requires true dedication and discipline, regardless of what markets are concerned about in the short run.

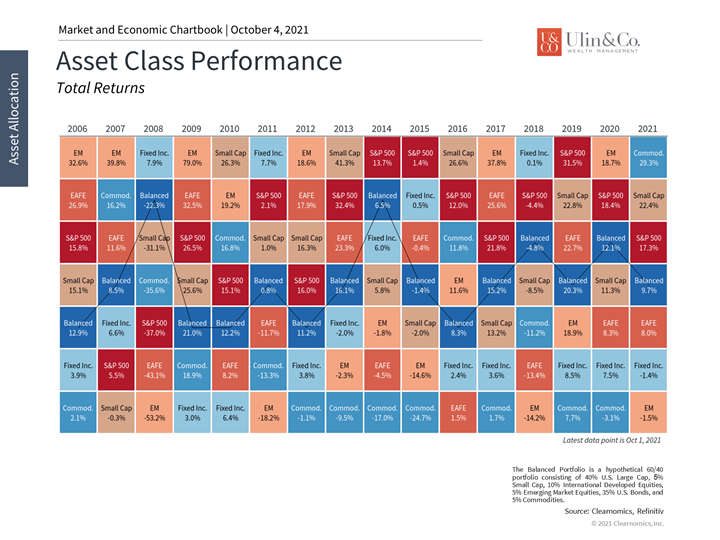

They say a picture is worth a thousand words, and in the stock market and economics that is definitely true. Having a few of our weekly charts on your wall or desktop can be a helpful reminder of where we have come over months, years and decades while putting this all in a better perspective.

The economic expansion is still strong

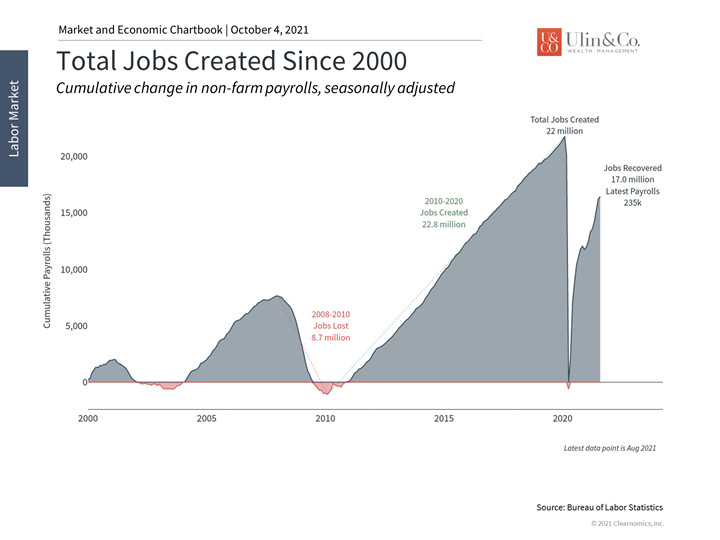

The economy is still growing rapidly 18 months after the unemployment rate peaked at 14.8%. U.S. GDP has surpassed pre-pandemic levels, as have corporate profits, and many measures of activity are at multi-decade highs. Despite investor fears, the underlying growth trends are still positive.

For many, jobs are the key metric since the pandemic directly impacted individuals’ ability to work and earn a living. Over 75% of the jobs lost during the pandemic have been regained and the unemployment rate has fallen to only 5.2%. While some sectors are still struggling to recover, others are struggling to hire workers fast enough. There are officially more job openings than unemployed individuals – an imbalance that is positive but that speaks to the changing nature of worker skills, job locations and more.

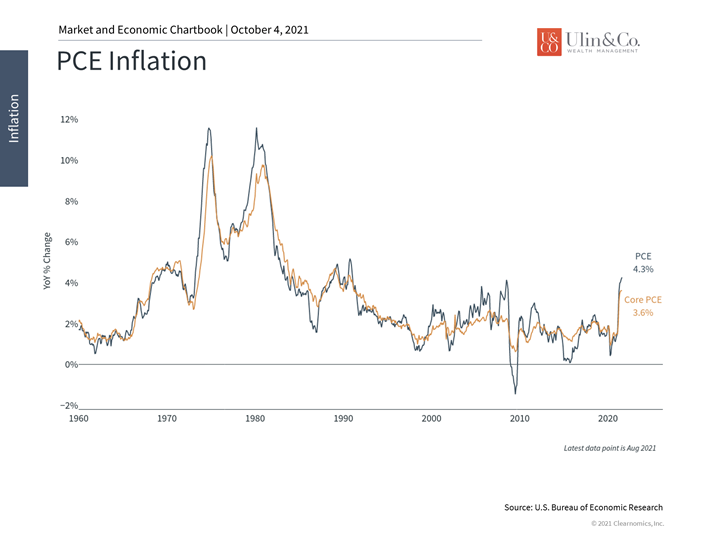

Inflation remains high and will depend on supply constraints

Inflation remains elevated across a number of traditional measures. The PCE inflation rate favored by the Fed, for instance, is at its highest levels since the early 1990s. The Fed itself has made it clear that their inflation targets have been reached, setting the stage for a reduction in asset purchases.

Many different factors are often referred to under the term “inflation.” Traditionally, inflation is seen as a monetary phenomenon. This made the 2010’s perplexing to many investors since vast amounts of monetary stimulus failed to materialize in the form of pricing pressures. Today, the biggest inflationary factors are the swift economic rebound and the on-going supply chain disruptions. While impossible to predict accurately, these effects will likely improve over time.

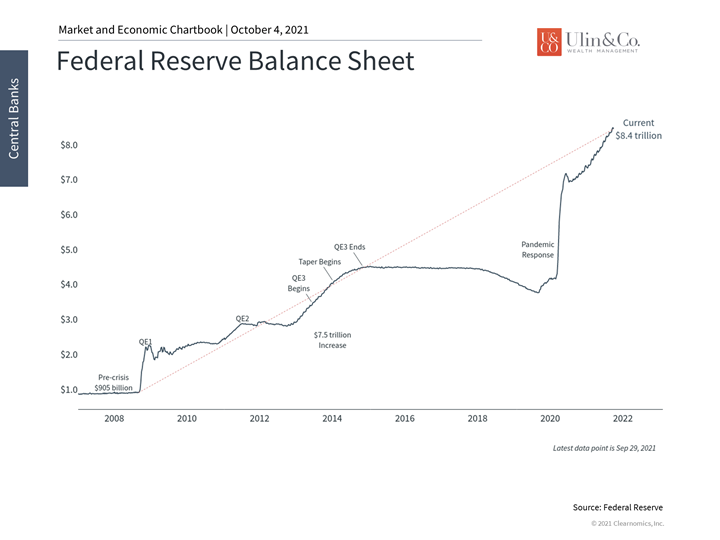

The Fed will likely begin tapering soon

The Fed will likely begin tapering its asset purchases in the fourth quarter. The central bank has been broadcasting this possibility for much of the year and has made it clear that tapering will be a gradual process that will last well into 2022. They have also communicated that rate hikes will require a different, more stringent set of criteria and will likely not begin until after their asset purchases end.

For investors, this means that there will likely be upward pressure on interest rates over a long period of time. Still, investors should not overreact to these gradual rate rises, especially given the extraordinarily low level of rates today.

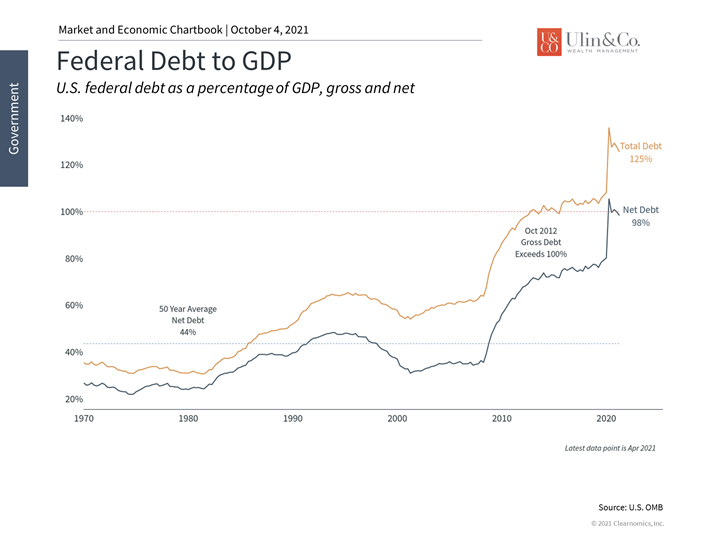

Government spending and the debt ceiling are front and center

Partisanship in Washington is on full display as a number of issues are being discussed. In the short run, the debt ceiling is the most pressing concern for financial markets which fear a repeat of 2011’s fiscal cliff scenario. In the long run, new spending proposals will have an important impact on infrastructure, taxes and more.

While these developments are important to watch, investors ought to maintain a long-term perspective on the impact of Washington policy on markets. Financial markets and portfolios have performed well across a variety of party leadership and tax regimes. Regardless of how one personally feels about new bills and proposals, it’s important to focus more on staying invested.

International markets still have diversification benefits

Although emerging markets have stumbled this year due to the delta variant and challenges in China, staying internationally diversified is still important. Many of the challenges around debt, shadow banking and regulation in China have been in focus for over a decade. And while these issues are coming to a head, the Chinese government is likely to be in a position to cushion any major fallout.

The bottom line? Investors must always balance risk with reward. Despite shifts in sentiment, staying invested and diversified are still the keys to achieving financial goals in Q4 and beyond.

The point is that for everyday investors who are planning for retirement and life goals, basing short term decisions on headline investor concerns would have backfired over the long history of financial markets.

For more information on our firm or to get in touch with Jon Ulin, CFP®, please call us at (561) 210-7887 or email jon.ulin@ulinwealth.com.

You cannot invest directly in an index. Past performance is no guarantee of future returns. Diversification does not ensure a profit or guarantee against loss. All examples and charts shown are hypothetical used for illustrative purposes only and do not represent any actual investment. The information given herein is taken from sources that IFP Advisors, LLC, dba Independent Financial Partners (IFP), and it advisors believe to be reliable, but it is not guaranteed by us as to accuracy or completeness. This is for informational purposes only and in no event should be construed as an offer to sell or solicitation of an offer to buy any securities or products. Please consult your tax and/or legal advisor before implementing any tax and/or legal related strategies mentioned in this publication as IFP does not provide tax and/or legal advice. Opinions expressed are subject to change without notice and do not take into account the particular investment objectives, financial situation, or needs of individual investors.