Fed Taper Tantrum Headlines Drive Volatility Concerns

When driving a car, you may only have a vague idea of how the underlying engine mechanism works. Internal combustion engines can contain any number of combustion chambers (cylinders), typically between four and twelve. Yet you should know that the accelerator speeds you up and the breaks slow you down.

When driving a portfolio construction strategy, you may only have a vague understanding of the underlying factors (cylinders) of bond risks and how they may affect your nest egg including interest rate risk, reinvestment risk, call risk, default risk and inflation risk.

Similar to basic concepts of automobile acceleration and braking, investors should develop fundamental knowledge of the mechanics of interest rates and how the Fed can affect the economy, lending rates and the markets.

The Fed Shifting Gears

A bit opposite of the effects of the accelerator and brakes on your car, when the economy is decelerating, the Fed downshifts short term rates (the Fed funds rate) into lower gears while adding a mountain of cash into the banking system through bond purchases (quantitative easing) to help “speed up” the economy while encouraging lending, spending and investing.

When the economy is accelerating back up along with inflation, the Fed up-shifts short term rates into higher gears while decreasing cash in the banking system to help slow down the economy (tapering).

While the Fed’s monetary toolkit controls short term rates, long term rates, as benchmarked by the 10 Year Treasury, are market driven. The 10-year T-note index is the most widely tracked government debt instrument in finance, and its yield is often used as the “holy grail” of benchmarks for other interest rates, such as U.S. mortgage rates.

Taper Tantrum Déjà vu?

Back in the summer of 2013 when then Fed Chairman Bernanke made an announcement during a congressional hearing (eight years ago this month) for the Fed to reduce its bond buying program, the notorious “Taper Tantum” evolved before the Fed even had a chance to take any action.

The benchmark 10-year Treasury yield spiked a full percentage point over the next few months to almost 3% causing many bond values to decrease into the red for the year. At the same time, the S&P 500 index relinquished -5% before turning around, and ended 2013 with what is still the best gain of the 21st century.

While the financial system has calmed down a bit this year since the pandemic led shutdown and stock market rollercoaster, many argue that it is overextended in many areas. In our opinion, there may be little the Fed can do to prevent another taper tantrum. The best it can do is be prepared and communicate clearly and consistently.

Stay on Course

After a rough start for bonds in Q1 with many fixed income indices still in the red as of today, markets have been trading on wobbly ground as investors watch and wait for the Fed to take action. With the announcement last week that it would soon begin to unwind its corporate bond holdings, some investors may wonder how this, and future Fed actions could affect their portfolios from both the stock and bond side of their equation.

For investors, this hints at the bigger question: when will the Fed begin to reduce the pace of Treasury and MBS purchases, which currently stands at $120 billion per month, and eventually raise rates? Expectations vary, but many believe the Fed will begin unwinding its balance sheet at the start of 2022 and raise rates in early 2023. But you never know what you may get.

This timing may change if inflation continues to heat up and the economy makes significant progress. Last week’s jobs report showed that the unemployment rate has already fallen to 5.8%. Moreover, when the Fed does begin to discuss these topics, many investors worry about another “taper tantrum” – a period in 2013 when the mere mention of reducing asset purchases rocked the bond market.

Although there is certainly the risk of another taper tantrum event, the following are three reasons for long-term investors to remain calm and stay on course.

First, as disruptive as the taper tantrum was to fixed income holdings, the typical diversified investor finished the year with strong gains. This is because the S&P 500 index generated a 32% return in 2013, offsetting the challenges faced by bonds.

Second, the Fed has (presumably) learned from that episode and will continue to bend over backwards to avoid a repeat. This means that they will either keep monetary policy loose for longer, or be extremely gradual in their approach. Of course, it can be argued that it may be better to rip off the band-aid, especially if there are excesses in the financial system.

Third, there is an old debate on whether “tapering is tightening.” In other words, is reducing the pace of bond purchases equivalent to selling bonds from its balance sheet? That is, is it the level or the direction that matters? While this is a theoretical debate, it’s clear in reality that the Fed will continue to be a significant buyer of bonds for quite some time. There are few reasons for long-term investors to worry about a sudden change in Fed policy.

Jon here. Regardless of how the Fed approaches tapering and tightening, long-term investors are better off staying focused on their financial goals rather than reacting to every Fed announcement and cryptic headline. Below are three charts that help to put monetary policy in perspective.

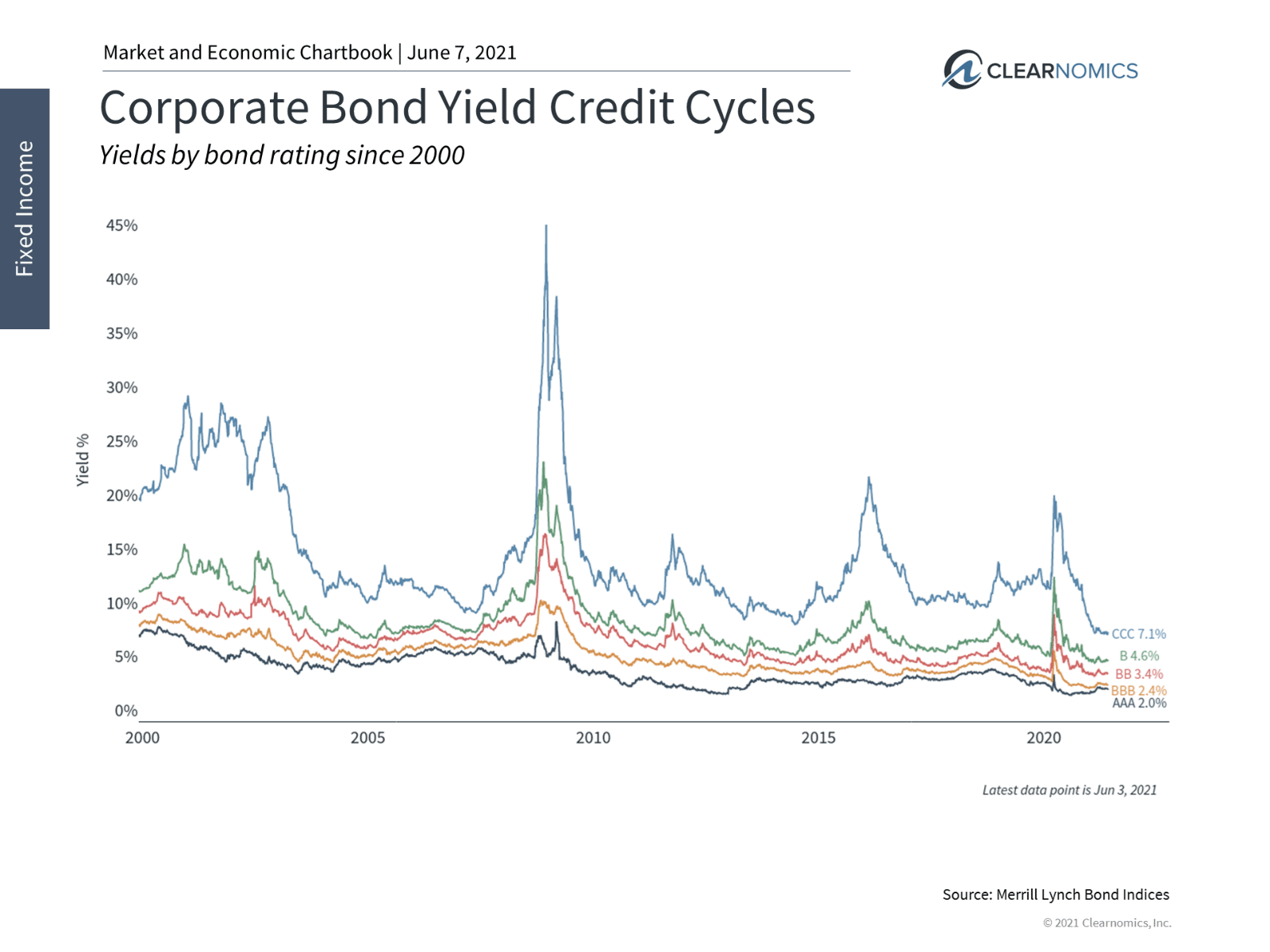

1 Fed action helped to calm the bond market last year

Credit markets began facing stress during the initial months of the pandemic. Actions by the Fed and Congress, and a quick recovery in the market helped bond yields to calm.

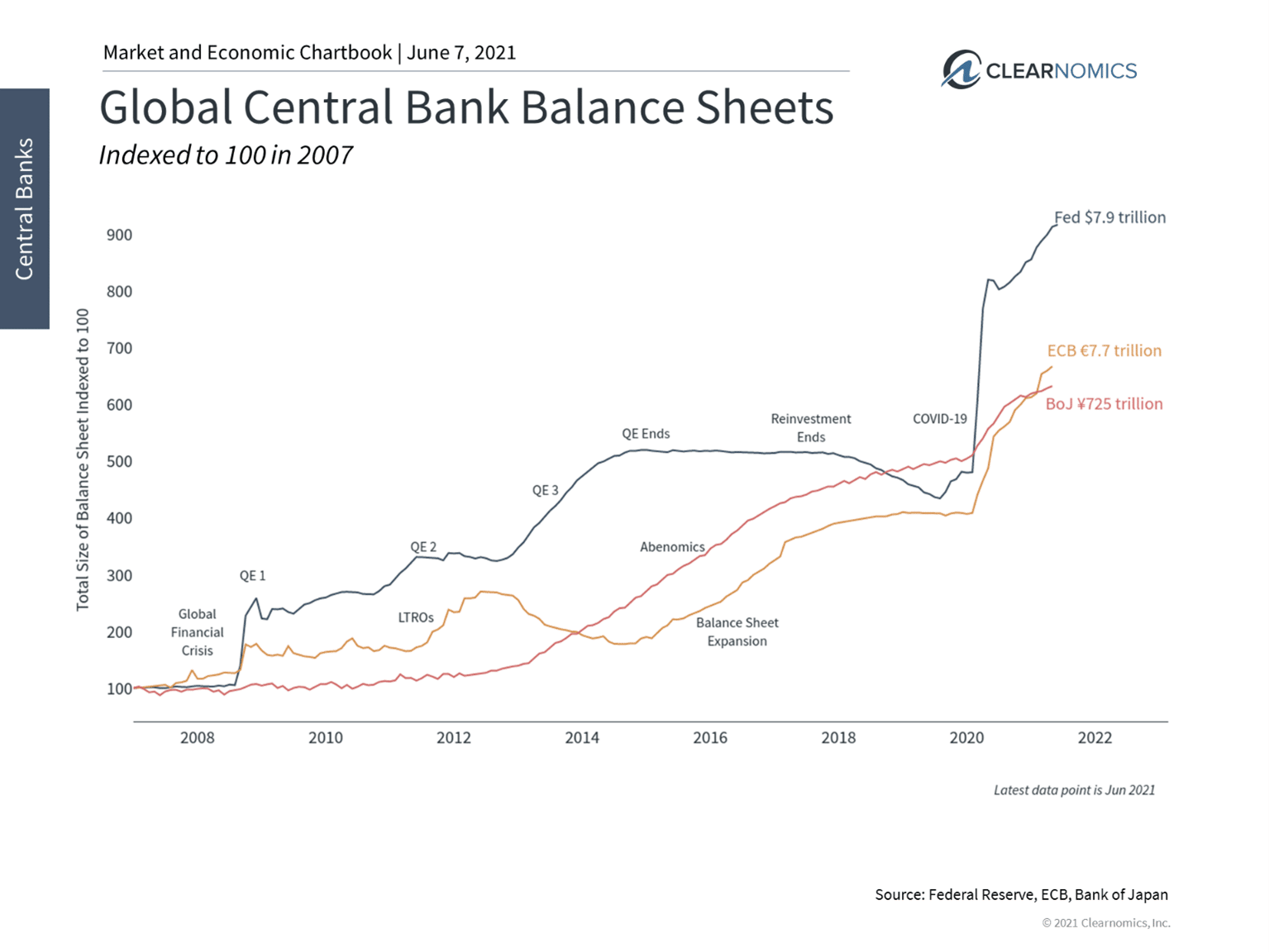

2 The Fed balance sheet is approaching $8 trillion

The Fed has expanded its balance sheet to nearly $8 trillion. This eclipses the $4.5 trillion reached after the financial crisis as well as the growth in the balance sheets of other major central banks.

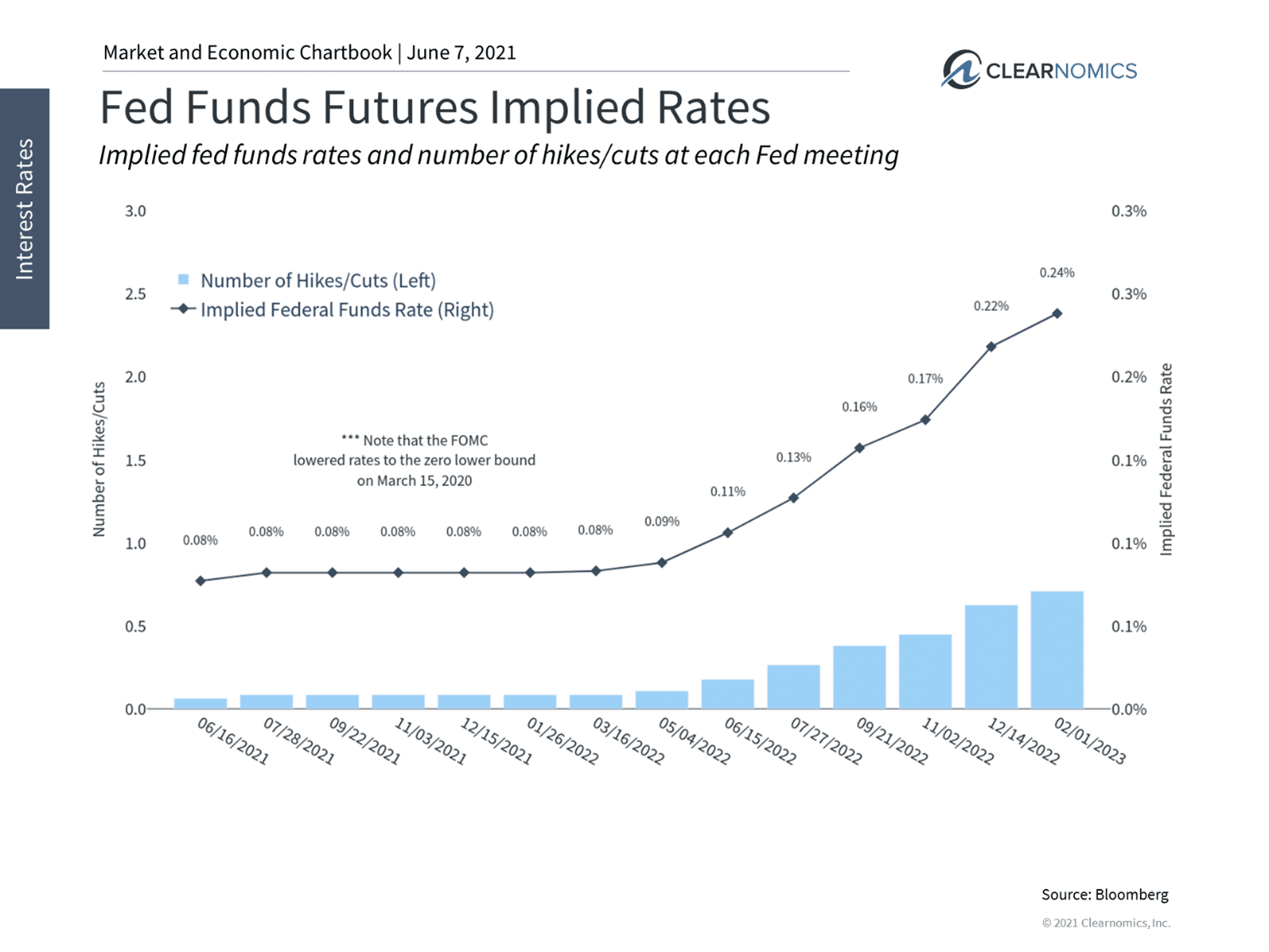

3 Markets expect Fed tightening over the next two years

At the moment, markets expect the Fed to begin raising rates in early 2023, and to possibly begin unwinding its balance sheet in early 2022. Of course, investors will watch for hints that these events could occur sooner.

The bottom line? Sitting near 1.5% today, we may see another point or so increase of the 10 year index this year fueled by a potential taper-tanturm, but will most likely not return anytime soon to the heights of the early eighties with near 16% rates

Investors ought to focus on their long-term financial goals rather than short-term Fed moves. Diversified portfolios have helped to conserve investors nest-eggs during the financial crisis, the taper tantrum and over the past 18 months – regardless of Fed policy.

For more information on our firm or to get in touch with Jon Ulin, CFP®, please call us at (561) 210-7887 or email jon.ulin@ulinwealth.com.

You cannot invest directly in an index. Past performance is no guarantee of future returns. Diversification does not ensure a profit or guarantee against loss.

The information given herein is taken from sources that IFP Advisors, LLC, dba Independent Financial Partners (IFP), IFP Securities LLC, dba Independent Financial Partners (IFP), and its advisors believe to be reliable, but it is not guaranteed by us as to accuracy or completeness. This is for informational purposes only and in no event should be construed as an offer to sell or solicitation of an offer to buy any securities or products. Please consult your tax and/or legal advisor before implementing any tax and/or legal related strategies mentioned in this publication as IFP does not provide tax and/or legal advice. Opinions expressed are subject to change without notice and do not take into account the particular investment objectives, financial situation, or needs of individual investors. This report may not be reproduced, distributed, or published by any person for any purpose without Ulin & Co. Wealth Management’s or IFP’s express prior written consent.

Securities offered through IFP Securities, LLC, dba Independent Financial Partners (IFP), member FINRA/SIPC. Investment advice offered through IFP Advisors, LLC, dba Independent Financial Partners (IFP), a Registered Investment Adviser. IFP and Ulin & Co. Wealth Management are not affiliated.