The Big Shortfall: America’s National Debt Reckoning

“Truth is like poetry. And most people hate poetry.” -Big Short

With the holy-grail 10-year Treasury note hovering near 5%—levels not seen since the dot-com era of the late ‘90s—attention is squarely on government spending and the ballooning national debt. This precarious situation raises concerns about a potential downgrade in the U.S. credit rating, rising borrowing costs, and a looming “black swan” event that could ripple across markets, reminiscent of major corporate bankruptcies from the past.

Let’s not forget: last summer, Fitch Ratings downgraded the U.S. Long-Term Foreign-Currency Issuer Default Rating (IDR) to ‘AA+’ from ‘AAA.’ The downgrade reflected anticipated fiscal deterioration, a growing debt burden, and governance erosion, as Congress repeatedly clashed over the debt ceiling.

What Does This Mean for Your Retirement?

As the national debt surges, future generations could face delays in Social Security benefits, later Medicare enrollment, or reduced payouts. This places an even heavier burden on the “three-legged stool” of retirement income—pensions, savings, and Social Security. For many, that stool may be down to just one leg: personal savings.

The Big Short Deux

With the Fed Funds Rate near its highest levels in 23 years, the government has spent nearly $1 trillion on debt service in the past year—up 30% from the prior year. Projections suggest this figure could hit $1.71 trillion in the next decade.

Jon here. While there’s no “funny math” akin to the mortgage-backed securities debacle depicted in The Big Short, one of my favorite movies, the parallels are eerie. A lack of oversight and rising complacency led to disaster in 2008. Today, mounting U.S. debt could trigger a similarly seismic reckoning.

Black Swans: When Rare Events Collide with Reality

Coined by Nassim Taleb in Fooled by Randomness, a “black swan” is a rare, unexpected, and catastrophic event that defies normal expectations but seems predictable in hindsight. These events—like the dot-com crash, the 2008 financial crisis, and the COVID-19 pandemic—have become more frequent.

As the U.S. debt approaches $36 trillion, the risk of a debt-driven black swan event grows, with consequences for individuals, corporations, and governments alike.

How the National Debt Impacts Investors

The national debt, now nearing $36 trillion according to the U.S. Treasury, has nearly quadrupled since before the 2008 global financial crisis. This relentless growth has fueled debates over budget deficits, the debt ceiling, and stimulus bills, raising questions about its implications for investors and the broader economy.

With the election now behind us, attention has shifted to the next administration’s cabinet nominations and policy proposals. The large and ever-growing national debt, and the complex ways it impacts the economy and markets, will only grow in importance. How can investors put government spending in perspective and stay focused on what drives markets in the long run?

The national debt has grown rapidly since 2008

When it comes to challenging issues like the national debt, it’s important to distinguish between what matters as citizens, voters and taxpayers, and what should matter as investors. As individuals, many rightly have strong personal and political views on government spending and taxation, and what it may mean for the country over the coming generations. This will likely hit headlines again when the debt ceiling, which is the maximum amount of debt the federal government is allowed to borrow, becomes a key issue when it’s reinstated in January 2025.

These concerns should be distinguished from whether the federal debt directly or indirectly impacts the economy and markets. Without diminishing the importance of the national debt, we need to keep in mind that markets have generated strong returns over the past two economic cycles. Investors should avoid overreacting with their portfolios at the expense of their long-term financial plans.

The size of the national debt relative to the size of the economy provides a clearer picture than the dollar amount of debt alone. There is no getting around the fact that the national debt has grown significantly, but the economy has also doubled since 2008. Specifically, the national debt now represents 120% of GDP. However, this includes debt the government owes to itself, i.e., Treasuries held by government agencies. Excluding treasuries, the government debt is 95% of GDP. This is still sizable and the latest jump is due primarily to pandemic-era stimulus.

It’s unclear where the limits of this borrowing are. Japan is the typical example of a developed country with a high debt burden that has exceeded 200% of GDP over the past 15 years, and over 250% since 2020. However, Japan’s situation is not directly comparable since it has a much bigger household saving rate, which helps to offset its significant government debt. Additionally, the U.S. economy is more diverse, demographic trends are much more favorable, and the dollar plays a far more important role in the global economy.

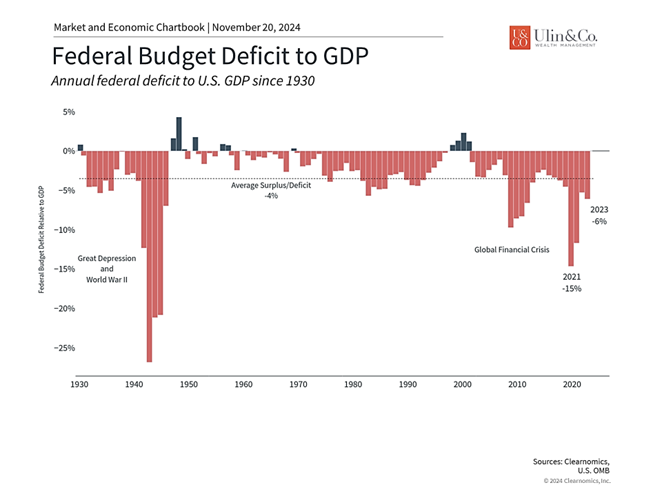

Large budget deficits each year have driven up the national debt

How has the federal debt increased so quickly? In two words, budget deficits. Budget deficits occur when the government spends more than it collects in taxes, which adds to the total debt. Taxes here include individual and corporate taxes, as well as social insurance taxes, such as those that fund Social Security, excise taxes, and others. The government also generates revenue from sources such as tariffs, but these are small by comparison, making up 2% or less of total government revenue each year.

Even though tax revenues tend to increase as the economy grows (even without raising tax rates), they have been outpaced by government spending over time. These expenditures have grown across what are known as “mandatory” programs such as Social Security and Medicare as well as so-called “discretionary” items such as defense and education.

The shortfall is funded by government borrowing, i.e., by issuing Treasury securities. Investors, institutions, and other countries buy these Treasuries and, in effect, fund the federal government.

The current deficit of around 6% of GDP is by no means small, but there have been many periods across history – primarily during economic downturns and wars – when the government has been forced to spend at these levels. History shows that, over time, deficits improve as the economy stabilizes, even if they don’t turn into surpluses.

The debt burden will only grow as interest payments rise

The unfortunate reality is that deficit spending does not seem to be going away, with neither major party focusing on the issue. The last balanced budgets occurred during the Clinton years and the Nixon administration before that. The accompanying chart shows that left unchecked, government projections suggest that interest payments on the debt alone could rise to $1.71 trillion in ten years.

About two-thirds of the national debt is held either by the government itself or by U.S. citizens. Other countries hold the rest with China owning about 2.2% of the U.S. government debt, although this proportion has declined. Many investors worry that growing debt levels means that Treasuries could be less attractive in the future. In the extreme, this could hamper the government’s ability to roll its debt, possibly leading to skyrocketing interest rates, or weaken the dollar’s standing as the world’s reserve currency. Ultimately, many worry that the U.S. could lose its position in the global economy.

While this is possible, it does not seem likely just yet, even with increased enthusiasm for dollar alternatives such as cryptocurrencies and gold. In fact, this has been a concern among economists for many decades. And yet, when the global economy faces distress, investors and governments turn to the U.S. as a safe haven. In 2011, for instance, when Standard & Poor’s downgraded the U.S. debt during the fiscal cliff standoff, investors didn’t sell their Treasuries – they rushed to buy more. Counterintuitively, this is because U.S. debt securities are still the standard for stable, risk-free assets in the world, despite these challenges.

Finally, and perhaps most importantly, markets have done well regardless of the exact level of the government debt and taxes over the past century. Ironically, the best time to invest over the past two decades has been when the deficit has been the worst. These periods represent times of economic crisis when the government is engaging in emergency spending, which tends to coincide with the worst points of the market. And while this isn’t exactly a robust investment strategy, it does underscore the importance of not over-reacting to fiscal policy in one’s portfolio.

The bottom line? The federal debt is a complex and controversial topic. As with many heated issues, it’s important for investors to separate their personal concerns and not react with their hard-earned savings or investments.

The onus is increasingly on individuals to navigate these uncertainties. Whether it’s building a robust retirement plan or staying diversified in the face of market shifts, a thoughtful strategy is key. As always, the best defense is a clear, disciplined approach to your financial goals.

For more information on our firm or to request a complementary investment and retirement check-up with Jon W. Ulin, CFP®, please call us at (561) 210-7887 or email jon.ulin@ulinwealth.com.

Note: Diversification does not ensure a profit or guarantee against loss. You cannot invest directly in an index.

Information provided on tax and estate planning is not intended to be a substitute for specific individualized tax or legal advice. We suggest that you discuss your specific situation with a qualified tax or legal advisor.

You cannot invest directly in an index. Past performance is no guarantee of future returns. Diversification does not ensure a profit or guarantee against loss. All examples and charts shown are hypothetical used for illustrative purposes only and do not represent any actual investment. The information given herein is taken from sources that are believed to be reliable, but it is not guaranteed by us as to accuracy or completeness. This is for informational purposes only and in no event should be construed as an offer to sell or solicitation of an offer to buy any securities or products. Please consult your tax and/or legal advisor before implementing any tax and/or legal related strategies mentioned in this publication as NewEdge Advisors, LLC does not provide tax and/or legal advice. Opinions expressed are subject to change without notice and do not take into account the particular investment objectives, financial situation, or needs of individual investors.