Trump’s Tariff War Turbulence – 10 Investor Insights

We’ve received more client calls this past week than during the early days of the 2020 pandemic crash. Concerns are rising. Headlines are blaring. The VIX “fear index” is spiking. And markets? They’re swinging wildly in response to renewed tariff threats from President Trump — like an airplane suddenly losing altitude — reigniting global trade war fears and fresh recession forecasts.

But amid the noise and motion sickness — and the daily shifts in policy direction from the White House — we’re reminding clients of a few essential truths to help restore perspective, discipline, and calm.

🤖 1. The Quants and ai are Running the Show

In today’s markets, nearly half of all trades during volatile periods are driven by algorithms and AI-powered high-frequency quantitative trading—not human decision-makers. These automated systems can create intense feedback loops just from interpreting posts on social media and exaggerated price swings that often have little to do with the underlying economic fundamentals.

With the quants and AI in the driver’s seat, the market can behave unpredictably, making it difficult for individual investors to navigate. This is why it’s more important than ever to understand how market dynamics are changing and stick to a well-thought-out strategy, especially when the noise is deafening, and market swings feel chaotic.

📊 2. Volatility Is the Price of Admission

Though it may not feel like it, sharp market drops are a standard feature of investing. The S&P 500 experiences an average annual intra-year decline of 14%, even during years that finish strong in bull markets. After two years of strong stock market performance with relatively low volatility, this year might feel like a wake-up call but is actually par for course.

This current bout of volatility isn’t rare—it’s just uncomfortable. There’s always a lingering sense that “this could be “the next big one”—a crash that makes optimism feel foolish, even when the long-term odds remain in your favor. But as Peter Lynch famously said, “Far more money has been lost preparing for corrections, or anticipating corrections, than has been lost in the corrections themselves.”

That’s why the biggest hurdle to reaching your financial goals isn’t expert forecasts by the media, interest rate models, or Fibonacci charts. It’s overcoming your own behavioral and emotional biases, staying disciplined, and sticking to a plan. Volatility isn’t optional; it’s the price of admission for long-term growth.

👥 3. Advice Matters Most in a Hurricane

It’s easy to manage your portfolio when markets are calm and rising. As the saying goes, “everyone thinks they’re a genius in a bull market.” But when volatility spikes and fear takes over, having a CFP® as your financial advocate and personal CFO becomes invaluable.

Countless studies show that the average investor underperforms both the market—and their own financial goals—by nearly 60% over time, largely due to emotional, short-term decision-making. This is where behavioral coaching and steady guidance from a skilled advisor come in. In fact, according to Vanguard’s Advisor Alpha study, working with a financial advisor can add as much as 3% per year in net returns—not by trying to time the market or picking hot stocks, but by providing disciplined planning, tax strategies, and emotional coaching during turbulent times.

A great financial advisor doesn’t just build a portfolio. They help ensure your strategy remains aligned with your long-term vision, keeping both your money—and your mindset—in the game when it matters most. The right guidance can help you weather the storm and stay on course for the long-term growth you need.

📺 4. Tune Out the Noise

Media and social platforms amplify panic. It’s their business model and helps grow their viewership. The real economy—jobs, earnings, and credit markets—remains intact, even if slowing.

Don’t let 24/7 news feeds hijack your mindset. Try tuning out the daily chaos and checking your portfolio less. (Or just watch more Netflix.) While your health affects your wealth, your wealth should not affect your health or emotional mindset.

🔎 5. Know What You Own

Reacting to every headline or checking your portfolio on the hour isn’t a strategy. Whether it’s a 401(k) or a brokerage account, don’t go in blind – or bury your head in the sand.

Take the time to understand your investments, how they’re performing year-to-date, and which benchmark is relevant. Spoiler: it’s probably not the S&P 500 or Nasdaq you hear about on the news. Many clients have been surprised by how well their diversified portfolios have held up so far in 2025—even as stocks, crypto, and other assets take a hit.

Now’s the time to review your statements and adjust your expectations—without panicking.

🛠️ 6. Don’t Set and Forget

At the start of 2025, we proactively reduced exposure to big-tech and lower-quality bonds after several years of outperformance driven by big tech leadership along with expected tariff war volatility. Anticipating increased volatility, we also repositioned some aggressive investors into more balanced, moderate allocations before Trump’s “Liberation Day” to better weather market swings.

In addition, we’ve been selectively increasing exposure to defensive sectors as well as to alternative investments — including structured notes, private credit, and private equity — where appropriate. These positions are designed to hedge against market volatility, enhance income opportunities, and improve long-term portfolio resilience without sacrificing growth potential.

It’s worth noting that over 30% of the S&P 500 is concentrated in big tech, accounting for nearly half of its overall volatility. That’s why it takes experience, creativity, and disciplined strategy to thoughtfully reduce exposure and correlation to tech, while still leaving room to participate in its upside when the next bull market resumes as part of a globally diversified portfolio.

📉 7. Don’t Bail on the Ride

Selling during a market panic is like jumping off a rollercoaster mid-ride — painful, poorly timed, and usually regrettable. You don’t just lock in losses; you risk missing the recovery that often follows when fear fades. History consistently shows that discipline outperforms panic. Market timing is a fool’s game — no matter how loud the headlines or how convincing the “this time is different” narrative may seem.

Investing isn’t about winning or losing in the moment. You still own the same number of shares whether the market is up or down. Losses only become real when you sell. The key is staying invested long enough to let the math, the markets, and time work in your favor.

It’s easy to forget the strength of the past two years of returns in moments like this. But perspective matters: nearly 85% of the time, markets are up, and they’ve historically stayed positive for years — and decades — at a time, despite countless so-called Armageddon events along the way.

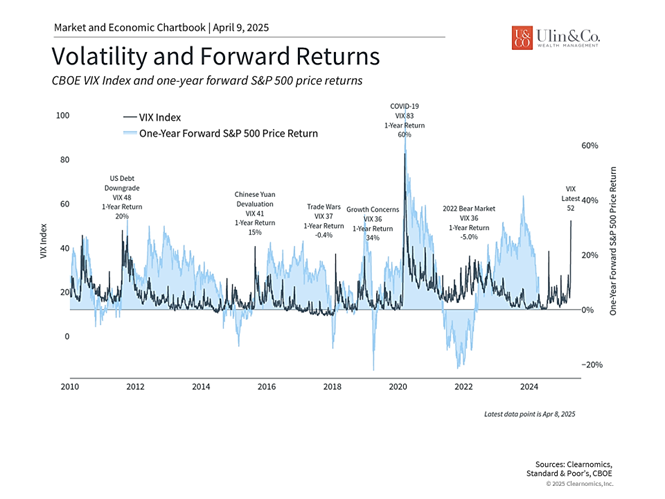

A perfect reminder for right now. Most of the time positive returns arise just after a catastrophic event causes stocks to go into correction or crash mode. The accompanying chart (below) shows that the VIX index, often known as the stock market’s “fear gauge,” can spike on a periodic basis. These peaks correspond to sharp drops in the market, such as in 2008 or 2020. These are times when markets are the most nervous and, in many cases, investors feel as if the situation will never stabilize.

This chart also shows the returns of the S&P 500 over the next year. As we discussed above, there is never any certainty about returns over any single year for the stock market. However, it’s clear that the greatest market opportunities often emerge exactly at the time when investors are the most worried. This is the heart of the famous Warren Buffett quote to “be fearful when others are greedy, and greedy when others are fearful.”

This is especially true if markets face liquidity rather than solvency concerns. Liquidity problems emerge when market declines force some investors – specifically those who use leverage, or borrowed funds – to sell other assets. In these situations, prices may decline even when the underlying fundamentals of an asset remain unchanged. These are classic cases where short-term market moves become disconnected from long-term outlooks, creating opportunities for patient investors.

It’s important to note that this is not an argument for market timing. Even when the VIX is high, there is no guarantee that markets will rebound quickly. Instead, investors should view this as additional support for taking a portfolio perspective. Market downturns often occur when valuations are the most attractive, and thus it can make sense to shift toward – not away – from these assets. Of course, what makes sense for a given portfolio depends on the specific circumstances.

🛡️ 8. Diversification Is Still Doing It’s Job

Headlines may scream “everything is crashing,” but our “all-weather” portfolios are doing what they’re designed to do. Diversification doesn’t eliminate losses—but it softens the blow. Think of it as an insurance policy: it won’t pay every time, but it often delivers when you need it most. Bonds, alternatives, and defensive sectors are stepping up.

In sports as well as investing, a winning strategy requires a combination of both offense and defense. Defense involves maintaining a portfolio that can withstand different phases of the market cycle. Stock market uncertainty and unexpected life events are inevitable, so always being ready to play defense is important. Two of the key principles of long-term investing are diversification and maintaining a long-time horizon.

This is showcased in the accompanying chart (below) which depicts the range of historical outcomes across stocks, bonds, and diversified portfolios. Moving beyond just one-year periods and a stock-only portfolio underscores why these are powerful ways to think about investing and financial planning. Diversifying might reduce the maximum returns an investor can experience, but it also reduces risk. This is evident in the balanced portfolio consisting of 60% stocks and 40% bonds. So far this year, the S&P 500 was 15% lower by April 8th, but a 60/40 mix of these indices has declined by nearly 5%.

After all, the goal is not to grow a portfolio at the fastest but most volatile rate, but to have the highest possible probability of achieving your financial goals. A diversified portfolio historically has a much narrower range of outcomes, allowing investors to better plan toward their goals.

Similarly, extending your time horizon by even a few years can have a significant impact on the range of outcomes. History shows that, since World War II, there has not been a 20-year period in which any of these assets and portfolios have experienced annual losses, on average. The same is true over 10-year periods for many diversified asset allocations. While this is only illustrative and is no guarantee of future performance, it clearly shows the importance of thinking long-term and having a diversified strategy in place.

🔍 9. Beneath the Surface, the Economy Is Resilient

We’re not seeing signs of a 2008-style meltdown, but rather a slowdown. Job growth, lending conditions, employment numbers, and consumer spending all remain solid, and inflation is slowly cooling off. The real economy is showing resilience beneath the surface—though market sentiment can sometimes paint a different picture.

If history repeats itself, we may see Trump walk back some (more) of his tariff threats—much like he did in 2018—potentially setting the stage for a rebound. With inflation easing, the inflationary pressures from tariffs may not be as severe as some experts predict. As the economy navigates these challenges, the underlying fundamentals appear stronger than the headlines suggest.

📉 10. A Reset Could Be What the Market Needs

After years of inflated valuations and rapid growth driven by big tech, this pullback from Trump’s Tariff War Turbulence might create the conditions for a more stable and investable market environment. The Trump Tariff situation may have put a brake on the meteoric rise of overvalued tech stocks, which had been fueled by optimistic promises and heavy capital spending on generative AI technologies.

We wouldn’t be surprised to see two quarters of economic slowdown or even a mild recession before the Fed considers rate cuts. In this environment, volatility may become the new normal—but with a disciplined, strategic approach, it’s far from something to fear. Rather than reacting to the noise, now is the time for strategic planning, not speculative moves.

Valuations are more attractive today after multiple years of strong stock market returns (see chart below). While it is still unclear where earnings will settle after accounting for tariffs, the price-to-earnings ratio of the overall S&P 500 has declined to 20.7x. Some sectors such as Information Technology, Communication Services, and Consumer Discretionary have seen multiples decline more amid the broader pullback.

The Bottom Line:

🧠 Volatility is uncomfortable—but not uncommon. JWU

Market corrections are part of the investing journey — not a reason to abandon a well-constructed plan. If your strategy made sense before President Trump’s tariff war tantrum, odds are it still does today.

Offense and defense are both important in times of market uncertainty. They help investors manage risk and take advantage of attractive opportunities that may emerge from short-term periods of market fear. In the long run, holding an appropriate portfolio is still the best way to achieve financial goals.

Whether or not this tariff war ultimately leads to a stronger economic environment for the U.S. in the years ahead remains to be seen. But history is clear: staying in cash and betting against the market has rarely worked out well over time.

There’s a saying that “the two best times to buy stocks are yesterday and today.” It’s a clever reminder that time in the market — not timing the market — is what drives long-term success. If you missed yesterday’s gains, don’t double down on the mistake by sitting out today.

This is when discipline matters most — when staying the course feels harder, but is more important than ever.

At Ulin & Co. Wealth Management, we’ve guided our clients through dot-com bubbles, financial crises, credit bubbles, flash crashes, pandemics, political turmoil — and now, tariff tremors. With more than two decades of experience, we’re here to help you navigate today’s uncertainty, and whatever comes next, with clarity, confidence, and a steady, experienced hand.

Thank you for your continued trust, confidence, and partnership. We’re always here when you need us — don’t hesitate to reach out. 📞 Have questions? Let’s talk.

For more information on our firm or to request a complementary investment and retirement check-up with Jon W. Ulin, CFP®, please call us at (561) 210-7887 or email jon.ulin@ulinwealth.com.

Diversification does not ensure a profit or guarantee against loss. You cannot invest directly in an index.

Note: This content is for informational purposes only and should not be construed as financial, legal, or tax advice. Please consult your financial advisor, attorney, or tax professional regarding your specific situation.

You cannot invest directly in an index. Past performance is no guarantee of future returns. Diversification does not ensure a profit or guarantee against loss. All examples and charts shown are hypothetical used for illustrative purposes only and do not represent any actual investment. The information given herein is taken from sources that are believed to be reliable, but it is not guaranteed by us as to accuracy or completeness. This is for informational purposes only and in no event should be construed as an offer to sell or solicitation of an offer to buy any securities or products. Please consult your tax and/or legal advisor before implementing any tax and/or legal related strategies mentioned in this publication as NewEdge Advisors, LLC does not provide tax and/or legal advice. Opinions expressed are subject to change without notice and do not take into account the particular investment objectives, financial situation, or needs of individual investors.