The Great Stock Rotation – A Breadth of Fresh Air

The past ten days have been nothing less than extraordinary with events that will go down in history. Former President Trump survived an assassination attempt by an inch, President Biden resigned from the 2024 race, cybersecurity company CrowdStrike caused massive global outages across industries that even grounded five major airlines, the Fed surprisingly stated they will soon cut interest rates with unemployment numbers ticking up, more banks are being stress-tested, and Nvidia fell nearly 13% into correction territory, dragging major tech stocks and indices down and along for the ride. It all sounds like the start of a scary movie.

With all eyes on the Fed Chair Powell along with every word out of is mouth, the last time the Federal Reserve cut interest rates was in March of 2020, cutting rates to near zero in response to the economic impact of the pandemic before historically hiking them up to 5.5% over the past couple of years to combat inflation. Achieving a soft landing after sustained monetary policy tightening is notoriously elusive and difficult to achieve but appears on course this time.

The Great Unexpected Stock Rotation

The recent stock market dynamics, particularly the unexpected rotation over the past week from large tech to non tech sectors, along with small-cap stocks that shot up themselves nearly 8% over the same time period as market breadth widens, provides a fascinating insight into how market sentiments and economic expectations can drive significant shifts in investment strategies.

Rotation brings to thought more so than sitting on a merry-go-round. A rotation phenomenon can be likened to various examples from music, art and fashion trends to even science. In scientific terms, consider the rotation of seasons. Each season brings distinct changes in weather patterns and ecological dynamics. Similarly, market rotations bring about changes in investment climates, where different sectors flourish or decline based on prevailing economic conditions.

For investors who may have hastily jumped into tech stocks in response to fear of missing out (FOMO) where sky high earnings may take a while to catch up to prices and the actual execution of generative ai innovation, the recent shift serves as a valuable lesson. Diversification, not only across different stocks but also across sectors and asset classes, remains a fundamental strategy to create a more smother, consistent return for investors. Investing in sectors that are currently undervalued or underperforming, but have solid fundamentals and potential for growth, can balance a portfolio and reduce risk.

Jon here. Good to know we have not received any investor panic calls over the last week with all the noise. With lower rates and inflation comes a second wind for many other “non-tech” sectors at lower valuations that may prove worthwhile for diversified long-term investors to remain patient and on course. As our client’s moderate risk balanced portfolios were already above benchmark returns in low double digit results for the first half of the 2024 and rolling quite a bit above that mark for the past 12 months, the exposure to small caps and other up-trending sectors already deployed into our strategies provided a solid buffer to the tech turbulence and did not make much waves in the weekly performance. As rates eventually get cut, inflation cools off, and the market breadth widens, we will continue to evolve our strategies in the second year of this post-pandemic bull market.

Broadening Market Changes

While much of the recent performance by the S&P 500 index has been driven by large cap tech stocks over the past 18 months, there are now signs that other parts of the market are benefiting as well. These shifts highlight the important fact that while investing trends may come and go, it’s the tried-and-true principles of investing that help investors grow their portfolios and achieve their financial goals over years and decades. Consider the following points to help keep you brain in the game and stay diversified while not chasing tech returns or returns in any asset class for that matter.

Performance is broadening beyond large cap growth

While investors tend to focus on major market indices and the one or two areas driving recent returns, the reality is that performance leadership tends to change over time. Large cap tech stocks have dominated headlines recently and for good reason – the Magnificent Seven stocks have gained 192% over the past year and a half. This is partly due to excitement over artificial intelligence breakthroughs, and partly because lower interest rates are generally positive for growth. This recent performance is also a reversal of the tech crash in 2022 when the Fed hiked rates.

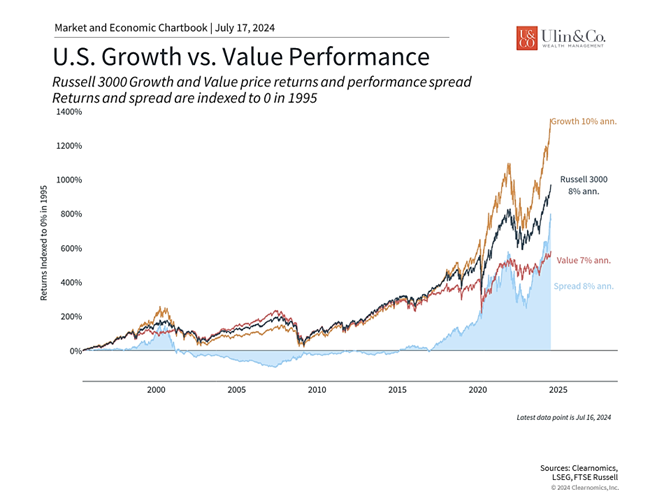

However, as the accompanying chart shows, there are now signs that other areas of the market are beginning to participate, with three important implications for investors.

First, recent economic reports confirm that inflation is improving which could lead the Fed to cut rates once or twice this year. This has propelled areas such as small cap stocks and large cap value. Small caps in particular tend to be more sensitive to interest rates since they represent less mature companies that often have more limited access to capital. Thus, the prospect of lower rates can be a catalyst for many of these stocks. These companies also tend to be more U.S.-focused, so they often outperform when there is positive news on economic growth.

Growth and value can each outperform over long periods with Stock Rotation

Second, value stocks have performed better recently due to these same factors. Notably, this has not been at the expense of growth stocks, per se. Instead, value stocks may be in the early stages of catching up after lagging for the past 18 months.

What exactly are value and growth stocks? While their exact definitions can differ among investors, these factors tend to be characterized by each stock’s valuation level. Those with lower valuations tend to be characterized as “value” while those with higher valuations are classified as “growth.” More broadly, value investors hope that a stock’s share price will adjust based on what it “should” be worth based on fundamentals such as earnings. Growth investors, on the other hand, hope that a company will continue to grow substantially, and are thus less concerned about the current valuation level or share price.

The accompanying chart provides historical perspective on how value and growth have fluctuated over time. In the late 1990s and early 2000s, growth stocks outperformed during the dot-com boom. This then gave way to strong outperformance of value stocks through much of the 2000s. This cyclical rotation from growth to value and back has occurred throughout history, driving much of the academic research around the value premium. So, while growth stocks have strongly outperformed most recently, history shows that leadership changes are not unusual.

Diversifying across styles helps to reduce portfolio risk

Finally, the outperformance of growth stocks does not mean that diversification is no longer relevant. In fact, the opposite is true: diversifying across styles allows investors to benefit from recent market trends while also protecting their portfolios from potential risks.

For example, the accompanying chart shows that those parts of the market that have performed well also have excessive valuations. The price-to-earnings ratio of large cap growth is now 28.4, driving the overall S&P 500 index P/E to 21.2. In contrast, large cap value only has a P/E of 15.7 while small cap value is far less expensive at 13.8. This is the case even though small cap value stocks are expected to experience earnings growth rates similar to large cap growth stocks over the next twelve months.

Performance has broadened across sectors as well. Ten of the eleven S&P 500 sectors have positive returns this year, with only the real estate sector slightly negative. Many sectors have year-to-date gains of 8% or more including financials, utilities, consumer discretionary, industrials, consumer staples, healthcare, and energy. While tech stocks have received most of the attention, and a few individual stocks have significantly outperformed the market, there are signs that other sectors are benefiting from the rally as well.

The bottom line? History shows that long-term investing isn’t just about “predicting winners” – it’s also about diversifying across styles, sectors, and more as we witnessed with the recent great stock rotation into small caps and other non tech sectors. Market leadership not only changes over time but also can do so swiftly. Staying diversified allows long-term investors to benefit from opportunities while also having a smoother ride as they work toward their financial goals.

For more information on our firm or to request a complementary investment and retirement check-up with Jon W. Ulin, CFP®, please call us at (561) 210-7887 or email jon.ulin@ulinwealth.com.

Note: Diversification does not ensure a profit or guarantee against loss. You cannot invest directly in an index.

Information provided on tax and estate planning is not intended to be a substitute for specific individualized tax or legal advice. We suggest that you discuss your specific situation with a qualified tax or legal advisor.

You cannot invest directly in an index. Past performance is no guarantee of future returns. Diversification does not ensure a profit or guarantee against loss. All examples and charts shown are hypothetical used for illustrative purposes only and do not represent any actual investment. The information given herein is taken from sources that are believed to be reliable, but it is not guaranteed by us as to accuracy or completeness. This is for informational purposes only and in no event should be construed as an offer to sell or solicitation of an offer to buy any securities or products. Please consult your tax and/or legal advisor before implementing any tax and/or legal related strategies mentioned in this publication as NewEdge Advisors, LLC does not provide tax and/or legal advice. Opinions expressed are subject to change without notice and do not take into account the particular investment objectives, financial situation, or needs of individual investors.

Advisory services offered through NewEdge Advisors, LLC, a registered investment adviser