The Dollar & Yuan on Wall Street’s Roller Coaster

Investing your money in the stock market is a bit like riding a major roller coaster. One minute you may be going 5 MPH uphill and the next minute you may be plummeting 70 MPH downhill.

No matter your age, vocation or what you may put down on an investment risk questionnaire, it’s only when the tracks turn sharply downward do you clearly see and recognize your own true colors and ability to stomach risk.

The VIX Index – often referred to as the market’s “fear gauge” had been ratcheting up to new heights in August along with gut-wrenching market swings in both directions on a daily basis.

After an unseasonably tranquil September, volatility from headline news from trade-wars, Brexit talks, impeachment threats, inverted yield curves and a decelerating global economy may spook the markets in October and come back with a vengeance like we saw in the fourth quarter of 2019.

While most investors “irrational exuberance” has become laden with “irrational anxiety,” no one can correctly predict the outcome of a potential trade war or when the next bear market will arrive.

Our goal as disciplined advisors and “financial psychologists” are to deter investors of all ages from jumping off a moving roller coaster or stock market, both of which could have dire consequences for their health or wealth. Successful investors understand the concept that to better reach their goals over time it’s about their “time in the market” and not “timing the market.”

For investors who focus too much of their time on day-to-day headlines and major economic forecasts, the fact that several market and economic concerns have become intertwined is a major challenge to digest.

The recent Fed rate cuts were partly in response to U.S.-China trade talks. In turn, both of these long-standing issues have conspired to strengthen the U.S. dollar and weaken the Chinese Yuan, leading the U.S. Treasury to designate China as a currency manipulator. Combined, all of these issues have increased market volatility and the perception of risk. How should disciplined, long-term investors interpret these events?

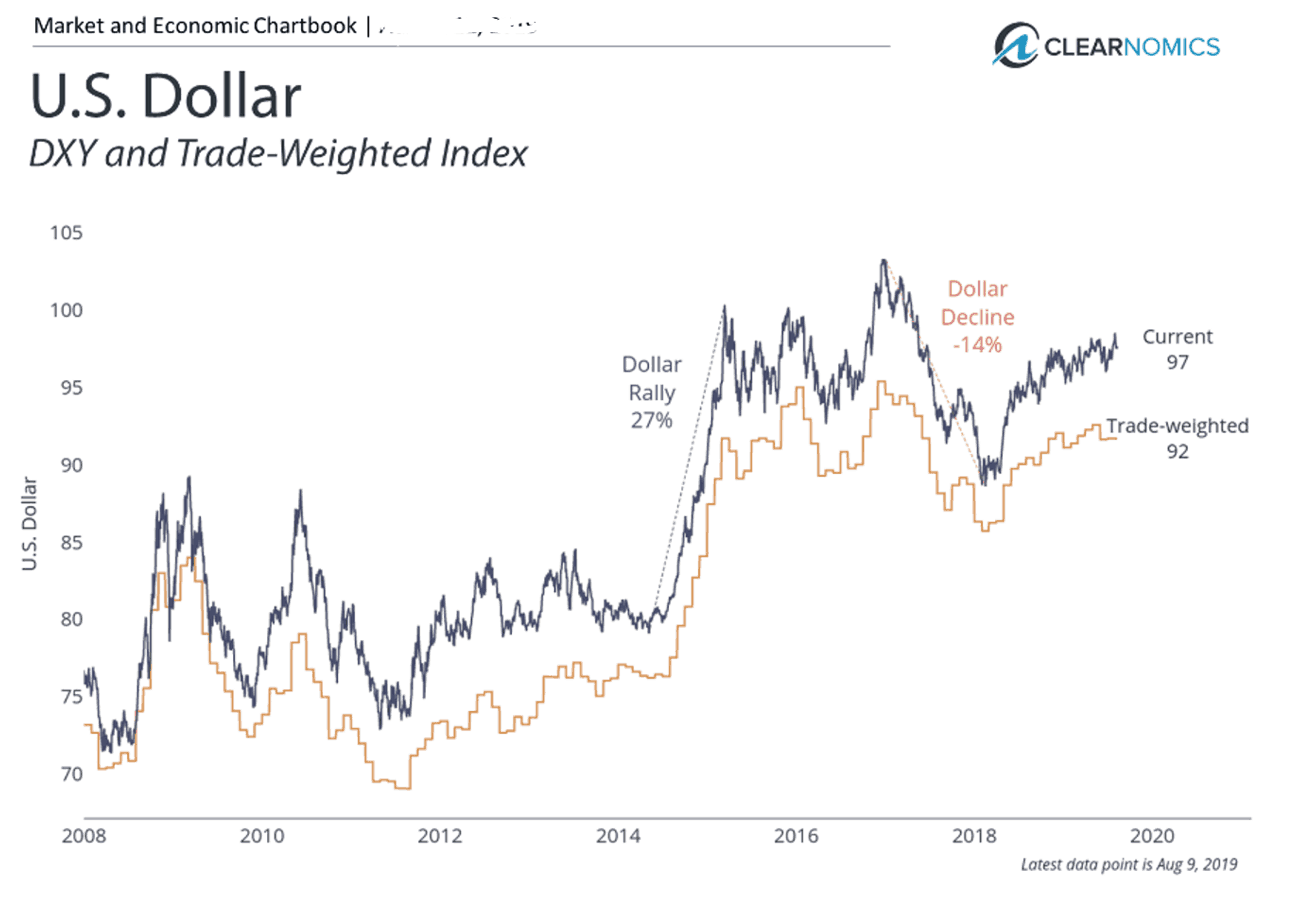

Currencies affect us in many ways. As consumers, the level of the U.S. dollar affects the prices at which we can import goods and services.

A stronger dollar means we can import more which helps U.S. consumers. However, for those who operate and work at multi-national companies, a stronger dollar may hurt sales because our goods and services become more expensive to foreign buyers. Thus, for countries who depend heavily on exports, a weaker currency can be beneficial.

The dollar remains strong amid global economic uncertainty

As investors, currencies are a valuable summary of the sea of macroeconomic data. All else equal, a country with stronger economic growth, higher interest rates, a healthier current account balance, among other factors, should have a stronger currency. The fact that currencies are always measured relative to one another means that the full global economic situation needs to be considered. In equilibrium, currency levels should reflect everything we know about the world.

To put this in perspective, four years ago China devalued its currency which sparked a global market correction. This was a result of slowing economic growth, extreme levels of debt, and fears of a so-called “hard-landing” in China. Although these fundamental issues were already known to investors and economists, it was the abrupt currency move that rippled across markets.

Today, the situation appears quite different. The recent devaluation of the Chinese Yuan and subsequent response from the Treasury Department most likely represent another round of escalating U.S.-China trade negotiation rather than something far worse. This isn’t to say that these events aren’t historic, or that trade issues couldn’t worsen further, but that this devaluation is quite different from what occurred in 2015.

What implications then, does this have for investors? From a currency perspective, the U.S. dollar has been strong over the past year and a half – one reason corporate earnings growth is expected to remain slow for some time. And while the devaluation of the Yuan has sparked some market volatility, the market is still less than 4% from all-time highs.

The bigger issue for most investors is that long-term interest rates have plummeted further. The 10-year Treasury yield, at only around 1.7%, is back to levels prior to the 2016 presidential election. Unfortunately, the search for yield will continue for some time for retirees, creating challenges for those who need income. The flip side is that mortgage and refinancing rates are low once again for those who can take advantage.

The bottom line for investors? Recent events from trade wars to the apparent deceleration of some market fundamentals have rattled markets but should be viewed with perspective. Unfortunately, there is still no relief for those investors who need portfolio income. All investors should continue to stay balanced, diversified and disciplined as we approach the 11th anniversary on March 9th, 2020 of the longest, and ‘most hated’ bull market in US history.

For more information on our firm or to get in touch with Jon Ulin, CFP®, please call us at (561) 210-7887 or email jon.ulin@ulinwealth.com. Get Started Today.

You cannot invest directly in an index. Past performance is no guarantee of future returns. Diversification does not ensure a profit or guarantee against loss.

The information given herein is taken from sources that IFP Advisors, LLC, dba Independent Financial Partners (IFP), IFP Securities LLC, dba Independent Financial Partners (IFP), and its advisors believe to be reliable, but it is not guaranteed by us as to accuracy or completeness. This is for informational purposes only and in no event should be construed as an offer to sell or solicitation of an offer to buy any securities or products. Please consult your tax and/or legal advisor before implementing any tax and/or legal related strategies mentioned in this publication as IFP does not provide tax and/or legal advice. Opinions expressed are subject to change without notice and do not take into account the particular investment objectives, financial situation, or needs of individual investors. This report may not be reproduced, distributed, or published by any person for any purpose without Ulin & Co. Wealth Management’s or IFP’s express prior written consent.