How to Hire the Right Financial Advisor in 2026

Why fiduciary, independent advice matters more than ever

If you’re searching for a fiduciary financial advisor or family office in 2026, you’re not alone. More investors, retirees, and business owners are rethinking who they trust with their money, and how they make that decision. The shift away from brand-driven advice toward independent, fiduciary planning is not a trend. It’s a response to a more complex financial world.

Twenty-five years ago, hiring a financial advisor often looked like buying a luxury brand. Investors chose brokerage firms the way they chose cars or universities, based on reputation and status. In the 1980s and 1990s, big wirehouse names and Wall Street prestige carried real weight. The firm’s logo and branding often mattered more than the person giving advice, and familiarity felt like safety.

That approach worked in a simpler investing world. Markets rose steadily through much of the 1990s, and making money felt easy. Then reality intervened. The dot-com collapse that bottomed in October 2002, followed just five years later by the global financial crisis beginning in late 2007, permanently reshaped how investors viewed risk and financial advice. That stretch, often called the “decade to forget,” also happened to be my first decade in this business, an education you do not get in college.

Today, that model feels outdated.

Investors are no longer searching for a firm name or a wirehouse logo. They are searching for the right financial advisor. Much like selecting a primary care or concierge physician, the decision has shifted from the institution to the individual. Credentials matter. Experience Matters. Incentives matter. Alignment matters.

How people actually arrive at an advisor

Most people do not hire a financial advisor in one dramatic moment. More often, the decision is triggered by a life event. A job change. Retirement. Starting or selling a business. An inheritance. Divorce. The loss of a loved one. These moments force decisions and expose gaps that were easy to ignore when life felt stable.

Just as often, the decision follows a series of conversations that leave people uneasy rather than informed. A tax meeting that explains last year but not what comes next. An estate plan that looks complete but raises new questions. A portfolio review that highlights returns without addressing risk or whether the plan still works. Business owners reviewing retirement or succession options frequently encounter complexity that leads to delay rather than action.

By the time families, retirees, entrepreneurs, and business owners reach out, they are rarely seeking more information. They already have plenty of that. What they want is clarity. Direction. Confidence to make better decisions.

This shift shows up clearly in how people search for advice today. In 2026, investors increasingly turn to advanced forms of ai layered on Google, Gemini, Vertex, Copilot, Perplexity, Grok, and ChatGPT, using precise terms like “fiduciary” and independent financial advisor. They are not casually browsing. They are trying to avoid costly mistakes.

Fiduciary and independent matter more now

The growing focus on fiduciary advice is not accidental. A fiduciary is legally required to act in your best interest. That standard matters most when decisions involve trade-offs rather than product selection.

Independence reinforces that obligation. Advisors who are not restricted to proprietary solutions tend to provide more objective and flexible guidance. This becomes especially important for retirees, business owners, and families managing complex financial lives.

Advice should evolve as your life evolves, not the other way around.

Financial advice feels more complicated today

Money decisions feel harder today. Not because people are less capable, but because the environment has changed.

People are living longer, which means retirement can stretch 25 or 30 years. Healthcare costs continue to rise and remain unpredictable. Interest rates spent much of the past decade near historic lows. Then bonds, including core holdings many retirees relied on for safety and income, went through one of the worst drawdowns in modern history.

Many conservative investors nearing or entering retirement followed the traditional playbook. They held bonds. They held cash. They reduced risk. Yet those strategies often failed to produce sufficient income and, in some cases, generated losses. Investors were then forced into an uncomfortable choice: accept lower income or take on equity risk they never intended to assume.

At the same time, financial lives have become more interconnected. Business owners and executives increasingly see personal and business finances overlap. Cash flow decisions influence retirement timing. Tax strategies affect Medicare premiums. Estate planning choices impact liquidity and income.

The real challenge today is not access to information. Information is everywhere. The challenge is knowing what matters most and in what order to address it.

Most professionals operate effectively within their specialties. CPAs focus on taxes. Attorneys focus on legal documents. Investment managers focus on portfolios. What is often missing is someone responsible for connecting the moving parts. That is where confusion builds and where costly mistakes tend to occur.

Why the role of a financial advisor has changed

Very few people hire a financial advisor today because they want stock tips or market predictions. Most already understand that predictions are unreliable and headlines change daily. What they want instead is perspective. How to hire the right Financial Advisor in 2026 starts with finding someone who helps them think clearly, weigh trade-offs, and connect decisions across their entire financial life.

In practice, the role now looks less like a traditional investment manager and more like a personal CFO. Someone who understands the full balance sheet. Someone who coordinates with accountants and estate attorneys. Someone who brings structure to complexity and filters out financial noise so families can focus on decisions that actually matter.

Investors are not looking for excitement. They are trying to avoid regret.

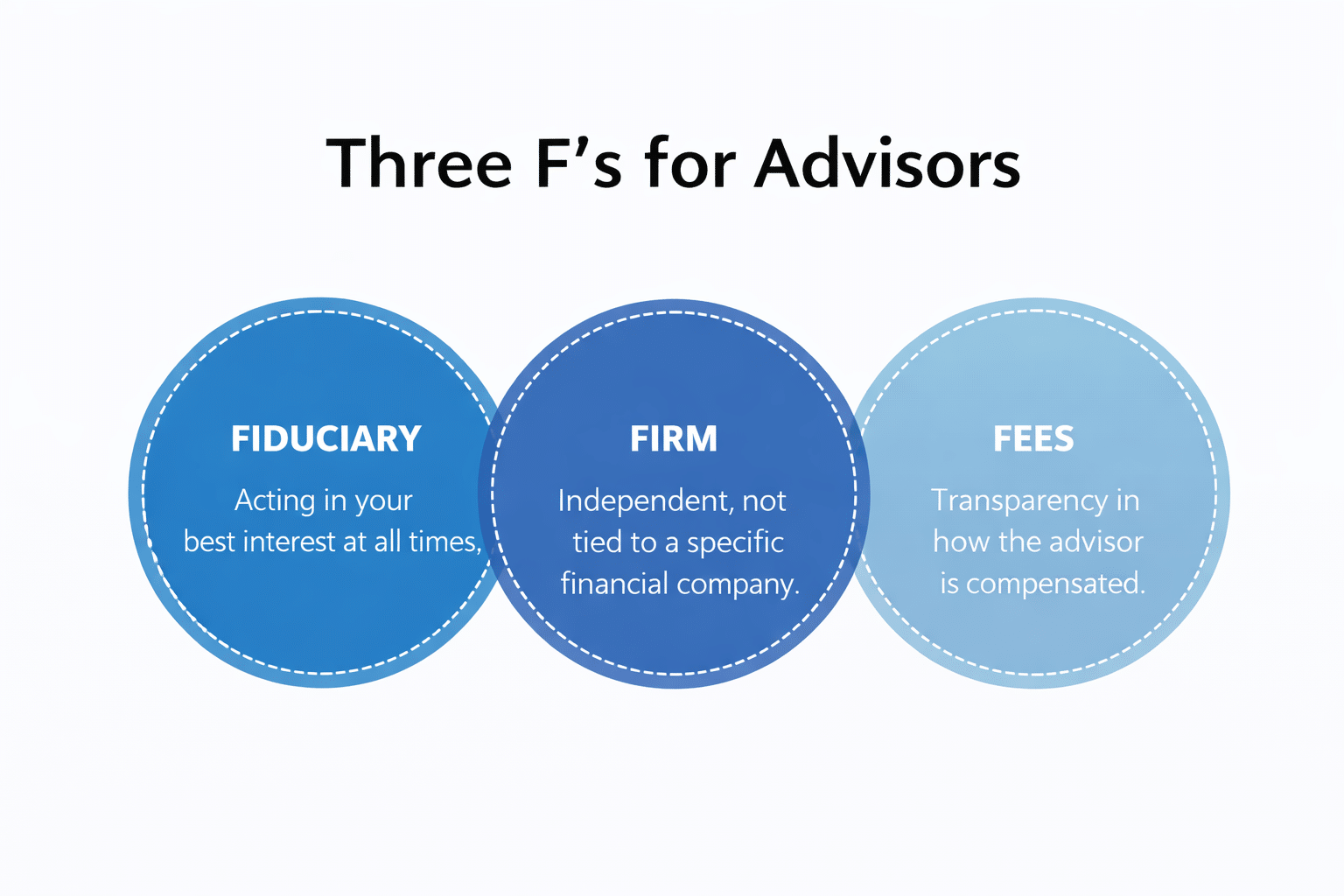

Follow the Three F’s to cut through the noise

With well over a million people offering some form of financial advice today, investors do not need more choices. They need a practical way to narrow the field.

A simple framework we suggest is the Three F’s.

First, fiduciary. Ask whether the advisor is legally required to put your interests first. Advisors holding respected designations such as CFP® typically operate under fiduciary standards with education, oversight, and accountability similar to other trusted professions.

Second, firm structure. Is the advisor independent or tied to a firm or product agenda? Independent Registered Investment Advisor firms generally operate under a fiduciary standard, allowing advice to fit your needs rather than steering you toward proprietary solutions.

Third, fees. How is the advisor paid? There is no free lunch in financial advice. Incentives matter. Fee-based or fee-only advisors are typically aligned with long-term planning rather than product commissions.

These filters will not answer every question, but they eliminate much of the noise and help separate long-term planning relationships from transactional sales models.

Experience shows up in outcomes, not predictions

After decades in this profession, experience stops being about forecasting markets. It becomes about recognizing patterns. You see where plans tend to break. You see how low interest rates reshaped retirement income assumptions. You see how bond losses pushed conservative investors toward uncomfortable choices. You see how longevity and healthcare costs changed what enough really means.

Generational differences stand out as well. Many Boomers benefited from higher yields and shorter retirements. Gen X and Millennial families face longer planning horizons, aging parents, complex career paths, and greater overlap between business and personal finances.

Advice that worked twenty years ago does not always translate cleanly today. Good advisors adapt without abandoning fundamentals.

The importance of fit and trust

Beyond credentials and structure, there is a human element that matters more than most people expect. A financial advisor often works with you through market cycles, career changes, retirements, and family transitions. They become an advocate when decisions feel heavy.

That relationship matters.

Much like choosing a primary care physician, you should work with someone you trust, relate to, and genuinely enjoy working with. Comfort affects how openly you communicate and how well plans get implemented. If conversations consistently reduce stress rather than add to it, that is meaningful information.

How to think about hiring an advisor in 2026

If you are evaluating an advisor this year, listen carefully to how conversations are framed. Do they focus on products or decisions? Are trade-offs explained clearly? Does the advisor ask thoughtful questions about your life rather than just your accounts?

Transparency builds trust. Clarity builds confidence.

For those who want a deeper framework, we created a Financial Planner Guide outlining questions many people do not think to ask until later in the process. It is designed to help investors make informed decisions, not rushed ones.

Final thought: How to Hire the Right Financial Advisor in 2026 is not about finding someone with perfect answers. It is about finding someone who helps you make better decisions over time, especially when the right choice is not obvious.

In a world where information is everywhere, judgment, alignment, and clarity are what people are really searching for.

If you are ready to start a planning conversation, the next step should feel straightforward, not pressured.

That is why fiduciary and independent advice matter more today than ever before.

For more information on our firm or to request a complimentary investment and retirement check-up, call (561) 210-7887 or email jon.ulin@ulinwealth.com.

Author: Jon Ulin, CFP® is the founder and Managing Principal of Ulin & Co. Wealth Management, an independent advisory firm based in South Florida for over 20 years. As a fiduciary wealth advisor, Jon helps successful individuals, families, and business owners nationwide with multi-generational planning, investment management, and retirement strategies. Learn more about Jon and our team at About/CV.

Start Your Journey Today

📍 301 Yamato Road, Suite 3150, Boca Raton, FL 33431

📞 (561) 210-7887 | 🌐 ulinwealth.com

Meeting Request

Work With a CERTIFIED FINANCIAL PLANNER™ The CFP® mark is the gold standard in personal finance, held by fewer than 100,000 U.S. professionals. Like a doctor or lawyer, CFP®s meet strict education and ethics standards to guide and protect your wealth. View Jon Ulin’s CFP® Board profile

Work With a CERTIFIED FINANCIAL PLANNER™ The CFP® mark is the gold standard in personal finance, held by fewer than 100,000 U.S. professionals. Like a doctor or lawyer, CFP®s meet strict education and ethics standards to guide and protect your wealth. View Jon Ulin’s CFP® Board profileMore Than Investing-Your Fiduciary Partner for the Long Run.

Our goal is simple: to help you live the life you envision—with clarity, confidence, and care. Most clients work with us for decades. Our average client tenure is over 15 years. We’ve also earned 20 five-star reviews on Google, reflecting our ongoing commitment to trust, transparency, and long-term results. Whether you’re a do-it-yourself investor, or simply looking for a second opinion, it starts with one conversation. Let’s explore how we can help you simplify, grow, and protect your wealth.

📍 Visit our Boca Raton wealth management firm at 301 Yamato Road, Suite 3150 — or schedule a Zoom consult. Call today: (561) 210-7887.

Barron’s rankings awarded in September 2025 based on prior 12-month data. Forbes/Shook rankings awarded in October 2025 based on data from 3/31/24-3/31/25. NewEdge Capital Group is the award recipient. Ulin & Co. Wealth Management & NewEdge Capital Group, LLC are not affiliated entities. Learn More.

Note: Diversification does not ensure a profit or guarantee against loss. You cannot invest directly in an index.

Information provided on tax and estate planning is not intended to be a substitute for specific individualized tax or legal advice. We suggest that you discuss your specific situation with a qualified tax or legal advisor.

You cannot invest directly in an index. Past performance is no guarantee of future returns. Diversification does not ensure a profit or guarantee against loss. All examples and charts shown are hypothetical used for illustrative purposes only and do not represent any actual investment. The information given herein is taken from sources that are believed to be reliable, but it is not guaranteed by us as to accuracy or completeness. This is for informational purposes only and in no event should be construed as an offer to sell or solicitation of an offer to buy any securities or products. Please consult your tax and/or legal advisor before implementing any tax and/or legal related strategies mentioned in this publication as NewEdge Advisors, LLC does not provide tax and/or legal advice. Opinions expressed are subject to change without notice and do not take into account the particular investment objectives, financial situation, or needs of individual investors.