4 Trump Policies to Navigate: Washington to Wall Street

Election seasons, especially those bringing a new president into the White House, can feel like a mix of high-stakes drama and reality TV, with news cycles amplifying every political twist. But should you pause your portfolio until the dust settles? The short answer: No. History shows that markets are driven more by macroeconomic forces—such as innovation, global conflicts, and demographic shifts—than by election outcomes or the identity of the sitting president.

Animal Spirits

President Trump’s inauguration marks a significant political shift amid market and economic uncertainty. The S&P 500 index fueled by animal spirits rallied nearly 5.3% in the month following the November election, before giving up all those gains by January 13th. As President Trump begins his second term, both Wall Street and Main Street are wondering what the next four years may bring.

Investors face a complex environment in 2025, with steady economic growth balanced against fewer Fed rate cuts, potential reinflation and high valuations. This sensitivity to growth policies may be stronger than in the past. While the president has already signed dozens of executive orders, many of the new administration’s policy details remain unclear, leaving room for significant changes in the coming weeks.

Taxes, trade, energy, and immigration will be key policy areas to watch, each with potential economic implications. Staying focused on fiscal spending, inflation, interest rates and the growing federal debt will be crucial for navigating the road ahead, no less the fate of the economy.

Presidents and Wall Street

It’s natural to feel uneasy about how presidential politics might impact your investments. Before letting headlines steer your decisions or personal feelings about Trump, keep in mind: personal and political feelings rarely mix well with portfolio management. Rash, short-term moves after a presidential election can derail long-term goals like retirement.

Here’s the bottom line: Every U.S. president since 1933—16 in total, evenly split between 8 from each party—has faced accusations of being the one to “ruin the economy” or “crash the market.” Yet time and time again, markets have proven more resilient, driven by economic fundamentals rather than political figureheads.

The numbers back this up. According to the Schwab Center for Financial Research, the S&P 500 posted positive returns in 17 of the past 23 presidential election years—a strong 74% of the time—with an average annual return of 7.1%. The outliers? Down markets during tumultuous times like the Great Depression in 1932, the dot-com bubble in 2000, and the financial crisis in 2008. These declines weren’t triggered by election results or by the sitting U.S. President, but by larger global events.

Overall: The economy has grown under both parties

When it comes to markets and the economy, presidents tend to receive too much credit and blame. History shows that economic growth and market rallies have occurred across both parties. This is because who occupies the White House is often less important than the decades-long business and market cycles that happen to be taking place.

So, while good policies do matter and can drive productivity and growth, there are many underlying factors that impact investors more than which party happens to be controlling Washington D.C.

4 Policy Areas to Watch: Wall Street Repercussions

Investors face a complex environment in 2025, marked by steady economic growth tempered by high valuations and fewer Fed rate cuts. While the president has already rolled out numerous executive orders, much remains uncertain about how policy decisions on taxes, fiscal spending, trade, energy, and immigration will shape the economy.

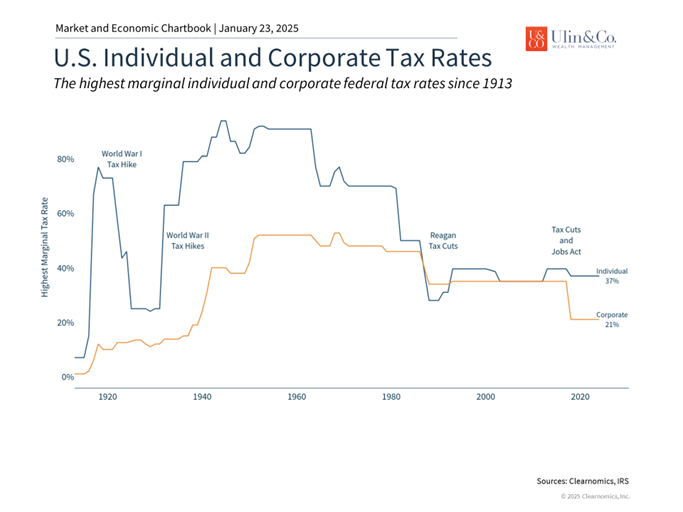

With a new Trump administration and Republican control of Congress, it is likely that much of the Tax Cuts and Jobs Act will be extended beyond its 2025 expiration. The political details of how this makes its way through Congress are still being debated, but this means that tax rates will likely remain low for individuals and businesses. This includes a highest marginal rate of 37%, corporate tax rates of 21% or lower, a higher estate tax exemption, and more.

1 The Tax Cuts and Jobs Act will likely be extended

While taxes have a direct impact on households and companies, they do not always have a straightforward effect on the overall economy and stock market. Tax rates represent just one element affecting economic growth, with numerous exemptions and provisions available to lower effective rates.

Current tax levels remain below historical averages. Given increasing national debt levels, prudent individuals should consider the potential for future rate increases in their long-term planning.

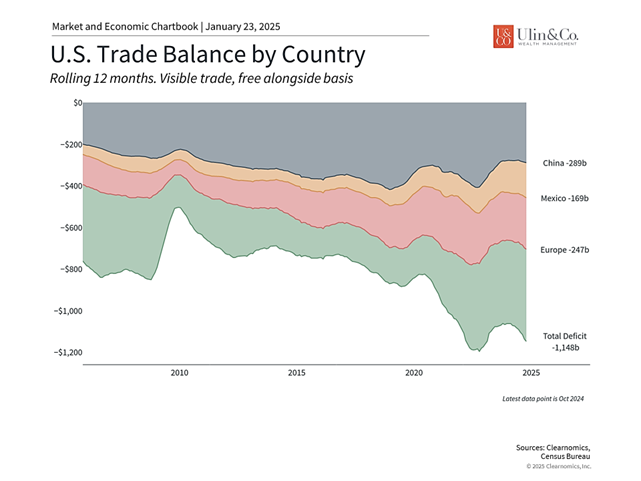

2 New tariffs could have a real economic impact

It’s important to remember that political rhetoric can differ from actual policies. Nowhere is this potentially more relevant than with trade. President Trump spoke on many occasions about his plans to impose a 10-20% tariff on all imported goods along with an additional 60% tariff on Chinese goods. More recently, he has discussed 25% tariffs on Canada and Mexico, saying on inauguration day that he will enact them on February 1. He also plans to establish an “External Revenue Service” to manage this tariff income.

During his first term, the Trump administration did in fact raise tariffs for many trading partners. This led to negotiations and trade deals including the United States-Mexico-Canada Agreement (USMCA) and the “Phase One” agreement with China. Many of these tariffs were then continued under President Biden.

The U.S. currently has the largest trade deficit in the world. As of November 2024, the U.S. imported $78.2 billion more than it exported. This is not necessarily a bad thing – it reflects the strength of the U.S. dollar and healthy consumer demand among Americans. However, this does mean that the country is effectively borrowing from the rest of the world.

Tariffs are a minimal source of government revenue, making up less than 2% of federal receipts each year. Many also worry that tariffs could contribute to inflationary pressures by raising the cost of imported goods entering the domestic market. From a political perspective, these concerns must be weighed against protecting sensitive intellectual property and preserving domestic manufacturing jobs.

3 Energy policy will promote drilling

Another key component of Trump’s agenda is the focus on energy security and dominance. He has already declared a national energy emergency and will create a National Energy Council to expand drilling in places like Alaska. According to the U.S. Energy Information Administration, the U.S. has produced more crude oil than any nation at any time for the past six years. The U.S. is also the world’s biggest gas producer and exporter of liquefied natural gas.

Oil and gas drilling is naturally politically controversial. The Biden administration recently banned drilling in parts of the Pacific and Atlantic Oceans, the Northern Bering Sea, and part of the Gulf of Mexico. Some of these bans have already been reversed, and Trump’s Interior Secretary has already vowed to reverse the rest.

For markets, greater energy supply could mean more stable prices, especially as geopolitical conflicts continue to rage around the world. Energy prices are also a primary driver of overall inflation. Recent increases in oil and gasoline prices have pushed headline inflation higher than the Fed would like.

4 Immigration will affect the job market

Politicians and the news typically focus on undocumented immigrants, especially with Trump’s immediate declaration of a national emergency on the southern border. However, immigration policy changes could impact legal immigrants as well, especially highly skilled workers. A reduction in immigration could have implications for the labor market, particularly in areas where worker shortages are already a concern.

There is disagreement within the Republican party over visas for skilled foreign workers, and the H1B visa program which enables companies to sponsor these workers has been a particular point of contention. Recent jobs data show that there are still 1.2 million more job openings than unemployed individuals, so immigration policy could have a significant impact on the economy in the coming years.

A more pressing commonality between both political parties than stock market growth is the ballooning U.S. debt, which, if left unaddressed, could lead to a future financial Armageddon. The U.S. national debt has been on a relentless upward trajectory, with debt held by the public reaching 98% of gross domestic product (GDP) in 2024. Projections suggest this figure could surpass the historic peak of 106%, set after World War II, by 2029.

In fiscal year 2024, the Biden administration and Congress spent $6.75 trillion, resulting in a $1.83 trillion deficit and bringing the total national debt to over $36 trillion. Looking ahead, forecasts indicate the debt could climb past $48 trillion by 2029. (US debtclock)

In response to this mounting issue, President Trump signed an executive order on January 20, 2025, establishing the Department of Government Efficiency (DOGE). Led by Elon Musk, DOGE’s mission is to modernize federal operations and reduce wasteful spending, with an ambitious target of cutting $2 trillion in federal expenditures. Thus far, the department has canceled $420 million in contracts and leases, but meeting its lofty goals remains a significant challenge.

Despite these efforts, neither party has successfully implemented lasting measures to control the debt. Tax cuts paired with higher spending have only worsened annual deficits, raising concerns about long-term economic repercussions if the debt spiral continues.

For investors, the implications of rising national debt are critical to watch. Escalating debt levels could drive changes in interest rates, inflation, and overall economic stability. Staying informed about fiscal policies and reforms will be essential for making sound investment decisions in this increasingly uncertain environment.

The bottom line? Political headlines may dominate the news, but markets tend to follow broader economic forces. While these 4 Trump Policies from taxes, energy, trade, and more can nudge markets in the short term, investors who focus on fundamentals and maintain a long-term perspective are better positioned to succeed.

Rather than letting politics drive investment decisions, focus on staying diversified, monitoring potential risks, and capitalizing on opportunities aligned with your personal goals. Remember, the most consistent driver of success in investing is not who sits in the White House, but how you manage your financial plan.

For more information on our firm or to request a complementary investment and retirement check-up with Jon W. Ulin, CFP®, please call us at (561) 210-7887 or email jon.ulin@ulinwealth.com.

Diversification does not ensure a profit or guarantee against loss. You cannot invest directly in an index.

Note: This content is for informational purposes only and should not be construed as financial, legal, or tax advice. Please consult your financial advisor, attorney, or tax professional regarding your specific situation.

You cannot invest directly in an index. Past performance is no guarantee of future returns. Diversification does not ensure a profit or guarantee against loss. All examples and charts shown are hypothetical used for illustrative purposes only and do not represent any actual investment. The information given herein is taken from sources that are believed to be reliable, but it is not guaranteed by us as to accuracy or completeness. This is for informational purposes only and in no event should be construed as an offer to sell or solicitation of an offer to buy any securities or products. Please consult your tax and/or legal advisor before implementing any tax and/or legal related strategies mentioned in this publication as NewEdge Advisors, LLC does not provide tax and/or legal advice. Opinions expressed are subject to change without notice and do not take into account the particular investment objectives, financial situation, or needs of individual investors.