$100 Oil and Hormuz: What Betting Markets Signal

Why This Energy Shock Isn’t 2022

Markets look remarkably calm for a conflict that threatens one of the most important oil routes in the world. Despite the U.S.- Iran war entering its third week, $100 Oil and Hormuz shutdown, investors appear to be betting the disruption will be short-lived. But if the Strait of Hormuz remains constrained and oil holds above $100 a barrel, that confidence could quickly be tested.

At that point the real question becomes whether policymakers can cushion the shock. Strategic reserves can steady markets temporarily, but they cannot replace a prolonged supply disruption that could lead to higher inflation and rates.

This isn’t 2022 déjà vu.

When oil spikes and war headlines dominate the news, investors quickly jump back to 2022. That year felt like a perfect storm. Russia invaded Ukraine. Oil surged toward $140. Inflation hit 9.1%. (U.S. Bureau of Labor Statistics). Stocks fell more than 20%. Bitcoin collapsed. Bonds delivered one of the worst years in modern history.

Should investors assume history is repeating and the same investing playbook is back? The short answer is no. The forces driving inflation and markets in 2022 were very different. Much of that inflation was fueled by massive pandemic stimulus checks and business aid programs, not oil alone.

It is also worth remembering how quickly energy shocks can fade. Oil peaked after the invasion but by December 2022 WTI had already fallen below $70.

Three shocks hit markets at once. Inflation surged after the COVID stimulus wave. The Fed launched the fastest rate hiking cycle since the early 1980s. Energy prices jumped after the Russia invasion. The war grabbed headlines, but monetary policy did most of the damage.

The Fed lifted rates from near zero to above 5% in roughly sixteen months. (Federal Reserve data) Liquidity vanished and every asset priced on cheap money had to reset. Stocks, bonds, and cryptocurrencies fell together.

That environment does not exist today. Inflation is running roughly half its 2022 peak and the Fed is holding rates high rather than launching another tightening cycle. The starting conditions are very different.

The Oil Shock Returns

Where the comparison to 2022 does rhyme is oil. U.S. and Israel strikes against Iran at the end of February pushed crude sharply higher, briefly sending prices above $115 before settling near $95. The initial shock has eased, but the real risk depends on the duration of this war, not the headlines.

The critical chokepoint remains the Strait of Hormuz, where roughly 20 million barrels of oil move through the channel each day, about 20% of global supply. Even the possibility of mine threats or shipping disruptions can force tankers to reroute and push insurers to raise war-risk premiums. (U.S. Energy Information Administration)

Markets do not wait for supply to disappear. They react to the risk of disruption.

Strategic reserves offer only temporary relief. The International Energy Agency recently announced a release of hundreds of millions of barrels from global reserves. That sounds enormous until you run the math. The world consumes nearly 100 million barrels of oil per day. A 400 million barrel release equals roughly four days of global demand. It can calm panic, but it does not solve a prolonged disruption. (International Energy Agency / EIA estimates)

Strategic reserves can calm markets temporarily. They cannot replace a prolonged supply shock. International Energy Agency member countries collectively hold about 1.5 billion barrels of strategic petroleum reserves, including the U.S. Strategic Petroleum Reserve. At current consumption levels that equals only about two weeks of global demand. (International Energy Agency)

Even if the Strait of Hormuz were disrupted, the world would not instantly lose every barrel moving through the channel. Saudi Arabia and the UAE can reroute limited supply through pipelines to the Red Sea and Gulf of Oman. But those routes handle only a fraction of the oil that normally passes through the strait.

The real issue is not production. It is evacuation. When tankers cannot leave the Gulf, oil backs up in storage. Producers are forced to cut output and global supply tightens quickly.Historically, the real economic pressure appears when oil rises toward $120 to $150 per barrel. At those levels fuel costs begin slowing economic activity and recessions often follow.

We saw this during the 1973 oil embargo, the 1979 Iranian Revolution, the 1990 Gulf War, and more recently after Russia’s invasion of Ukraine when oil briefly reached about $140 before falling below $70 within nine months. (U.S. Energy Information Administration)

These episodes followed a similar pattern seen in many geopolitical crises from the 1967 Arab-Israeli war to the 2003 Iraq invasion: the initial shock drives prices sharply higher, but markets eventually stabilize as supply adjusts and demand slows. Markets rarely run out of oil. Prices rise until demand slows enough to restore balance.

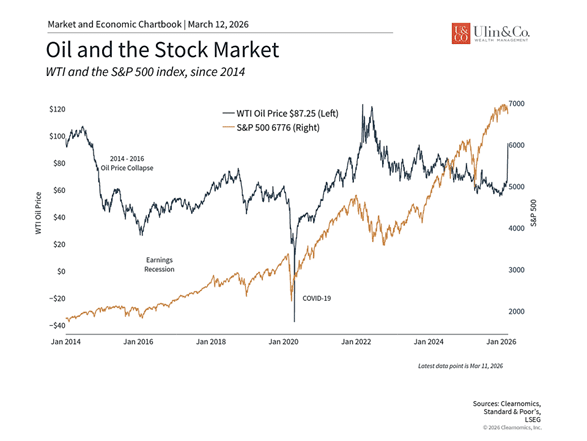

Why oil has climbed to nearly $100

It is often thought that when oil prices rise above $100, the economy starts to falter, affecting household budgets and inflation. Yet, it’s important to keep these moves in perspective.

If tensions persist and shipping becomes more complicated, oil could remain in the $90 to $110 range. (see chart) That level does not break the global economy, but it does influence inflation expectations and interest rate policy. If oil rises, inflation follows and rate cuts get pushed further out. Markets care far more about those forces than the conflict itself. War headlines move markets for days. Oil, inflation, and interest rates move them for years.

Three concerns keep resurfacing. First is disruption at the Strait of Hormuz, where roughly a fifth of global energy flows. Second is duration. The longer the conflict lasts, the harder it becomes to dismiss the economic consequences. Third, and often overlooked, is the machinery that moves global trade: shipping insurance, freight rates, and war-risk coverage. That is how a regional conflict becomes a global invoice.

This has a domino effect on the energy market. Without tanker transportation through the Strait of Hormuz, large Middle East oil producers have had to store oil instead. As storage facilities fill up, countries including Saudi Arabia, Iraq, Kuwait, Qatar, and the UAE have been forced to cut production. Unlike the typical OPEC production cuts to boost prices, these emergency measures are involuntary. This chain of events is why oil prices have risen so much in such a short amount of time.

For investors looking for signal instead of noise, three indicators matter most: whether ships continue moving through Hormuz, whether shipping insurance and freight rates spike, and whether rising energy costs push interest rate expectations higher.

Moments like this tend to follow a familiar pattern. Headlines escalate, fear spreads, and the instinct is to act. More often than not, that instinct leads investors in the wrong direction. A better approach is surprisingly simple.

Betting Markets Are Watching the Iran Conflict

Investors increasingly watch prediction markets for geopolitical signals. Platforms such as Polymarket allow traders to wager on real world outcomes, and those prices translate into implied probabilities.

Right now the odds point to a longer conflict, not a quick resolution. The “Venezuela II” scenario we discussed last week may be off the table. Traders place the probability of a U.S.–Iran ceasefire by May 1st below 40%. By December 31st the odds rise to roughly 77%. In simple terms, the market expects a ceasefire eventually, but not in the next few weeks.

Prediction markets often move faster than polls or analyst forecasts because participants risk real money. Research shows these markets correctly predict outcomes roughly 90% of the time one month before resolution and close to 94% as events approach.

For investors the message is simple. Markets are not pricing a short conflict. They are pricing uncertainty that could last months. In markets, duration matters far more than headlines.

Core Inflation vs Headline Inflation from $100 Oil and Hormuz Shutdown

Inflation had already begun cooling before the latest energy shock. Falling gasoline prices helped push headline CPI lower over the past year. That was the easier part of the inflation fight.

The harder part remains underneath. Core inflation, which excludes food and energy, has flattened and now sits slightly above headline CPI (see chart below). The remaining pressure sits in housing, insurance, healthcare, and services. These sectors rarely fall quickly.

Higher oil prices affect far more than the gasoline pump. While national gasoline prices have climbed back toward roughly $3.50 per gallon, still well below the $5 peak seen four years ago, energy costs ripple through the entire economy.

Transportation, manufacturing, and logistics all rely on energy. When oil rises, the cost of moving goods, producing materials, and powering businesses rises as well. Economists refer to this as cost-push inflation, where higher production costs eventually get passed through to consumers.

Energy shocks therefore layer on top of existing inflation pressures rather than replacing them. If crude remains elevated for several months, headline inflation rises and the Federal Reserve becomes more cautious about cutting rates. This is the real risk. Not a repeat of the 9% inflation shock from 2022, but inflation stalling closer to 3.5% to 4%. If that happens, the Fed does not need to raise rates again. It simply delays cutting them.

That scenario keeps the 10-year Treasury yield in a higher range, perhaps around 4.25% to 4.75%. In that environment bonds do not collapse the way they did in 2022, but they may not rally either. Fixed income returns come mostly from income rather than price gains.

After a painful stretch for bonds, with the Bloomberg U.S. Aggregate Bond Index underwater from 2020 through 2024 and putting pressure on traditional 60/40 portfolios, higher inflation could again challenge bond returns in 2026 and keep mortgage and other lending rates elevated.

Market Rotation Is the Real Story

The larger shift in markets is happening elsewhere and will again be front and center once the war and oil debacle cools down. The dominant story of the past two years was concentration. A small group of mega cap technology companies drove a large share of market returns. At one point the ten largest stocks represented roughly 35% of the S&P 500 according to data from S&P Dow Jones Indices.

That level of concentration rarely lasts. Leadership eventually collapses or broadens. What we have seen since last autumn looks more like rotation. Mega cap tech stocks have cooled after a huge run. Meanwhile other sectors are gaining traction.

Energy and materials are rising with oil. Industrials and infrastructure are strengthening. International markets have begun outperforming after years of lagging U.S. stocks.

Markets can weather higher oil prices

This is why sectors tied to the physical economy have started to lead. Our tactical focus for our diversified strategic balanced client portfolios remains on what we call HALO sectors. Heavy assets with low obsolescence risk. Materials, energy, industrials, infrastructure, and staples tend to benefit when inflation stays sticky, and leadership rotates away from high growth technology.

Coincidentally enough, these sectors are the place to lean-into during a situation like the current war and oil -energy situation, in addition to deploying into sectors such as aerospace and defense, cybersecurity and commodities stocks and funds.

Despite these historical lessons, the reality is that financial markets can react to oil price shocks in the short run. The S&P 500 is only down a couple of percentage points year-to-date, but many headlines are highlighting the South Korean KOSPI index’s decline of 17%, Japan’s Nikkei index’s 10% fall, and others since the end of February.

At the same time, energy companies benefit from higher prices. The energy sector has gained about 25% year-to-date and leads the market, just as it did in 2021 and 2022. Similarly, the commodities asset class has risen over 20% this year, driven both by energy and precious metals. This is not to say that investors should focus only on energy, but is a reminder of the benefits that holding different asset classes and sectors can have on portfolios. (Source: Bloomberg market data)

Recent events do create uncertainty on what the Fed may do next. If inflation rises due to higher oil prices, the Fed may need to keep rates higher than currently expected. At the moment, market-based measures expect at least one rate cut this year in September, and possibly two by the end of the year. However, if the supply disruption proves temporary, even if it lasts for months, its impact on monetary policy may be limited, just as it has been across history.

Of course, this doesn’t mean markets won’t continue to experience daily swings. Instead, it’s a reminder that properly-constructed asset allocations and financial plans are designed precisely to handle these types of risks. Making dramatic portfolio changes in response to headlines is often counterproductive. Successful investing is more often achieved by maintaining balanced portfolios and staying focused on long-term financial plans.

The Bottom Line: $100 oil and Hormuz shutdown from the Iran war does not resemble the shock of 2022. That year was driven by a rapid Fed tightening cycle that repriced every asset simultaneously.

Today’s environment looks more like a late cycle rotation layered with a geopolitical energy shock. Oil may strengthen inflation pressures if the conflict persists and delay rate cuts. But the broader market story is still shifting leadership rather than systemic collapse.

Investors should expect higher volatility, a wider range for interest rates, and continued sector rotation. Diversification matters more than headlines. The market is not repeating 2022. It is adjusting to a new phase of the cycle.

For more information on our firm or to request a complimentary investment and retirement check-up, call (561) 210-7887 or email jon.ulin@ulinwealth.com.

Author: Jon Ulin, CFP® is the founder and Managing Principal of Ulin & Co. Wealth Management, an independent advisory firm based in South Florida for over 20 years. As a fiduciary wealth advisor, Jon helps successful individuals, families, and business owners nationwide with multi-generational planning, investment management, and retirement strategies. Learn more about Jon and our team at About/CV. or call (561) 210-7887.

Note: Diversification does not ensure a profit or guarantee against loss. You cannot invest directly in an index.

Information provided on tax and estate planning is not intended to be a substitute for specific individualized tax or legal advice. We suggest that you discuss your specific situation with a qualified tax or legal advisor.

You cannot invest directly in an index. Past performance is no guarantee of future returns. Diversification does not ensure a profit or guarantee against loss. All examples and charts shown are hypothetical used for illustrative purposes only and do not represent any actual investment. The information given herein is taken from sources that are believed to be reliable, but it is not guaranteed by us as to accuracy or completeness. This is for informational purposes only and in no event should be construed as an offer to sell or solicitation of an offer to buy any securities or products. Please consult your tax and/or legal advisor before implementing any tax and/or legal related strategies mentioned in this publication as NewEdge Advisors, LLC does not provide tax and/or legal advice. Opinions expressed are subject to change without notice and do not take into account the particular investment objectives, financial situation, or needs of individual investors.